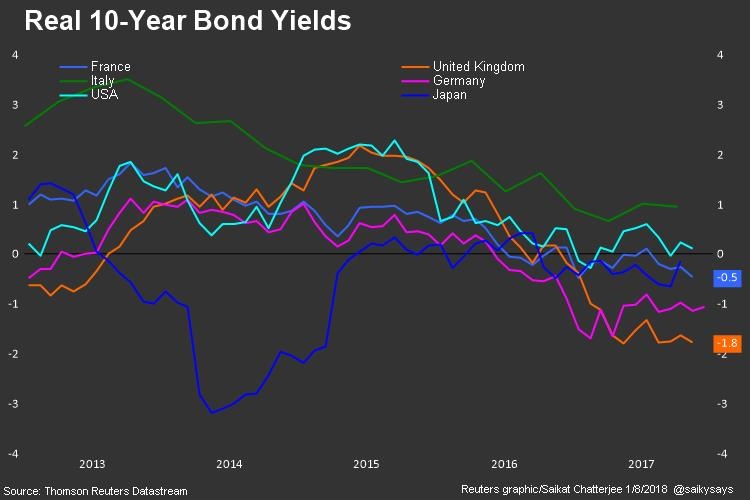

Negative real borrowing costs add fuel to markets that are already on fire, limiting the downward pressure on bonds, keeping corporate spreads on the tight side and pushing stocks to new high after new high. [...]

For investors, it’s a chicken and egg scenario. They’re crying out for policy “normalization” - higher rates and less central bank “interference” in markets - but are enjoying the asset price boom that’s in large part a direct consequence of central bank largesse.

E.g. news from July this year:

Greece is scheduled to end nearly a decade of external help this August, after implementing more than 400 policy measures demanded by creditors. The yield on the 10-year government bond has fallen about 30 basis points in the wake of the recent debt deal. It moved from standing at about 4.2 percent to 3.9 percent. In contrast, Italy’s 10-year yield currently stands at 2.668 percent and the U.S.’ at 2.85 percent.