Gode and Sunder (1993) recorded a result similar to yours. The abstract of the paper reads:

We report market experiments in which human traders are replaced by "zero-intelligence" programs that submit random bids and offers. Imposing a budget constraint (i.e., not permitting traders to sell below their costs or buy above their values) is sufficient to raise the allocative efficiency of these auctions close to 100 percent. Allocative efficiency of a double auction derives largely from its structure, independent of traders' motivation, intelligence, or learning. Adam Smith's invisible hand may be more powerful than some may have thought; it can generate aggregate rationality not only from individual rationality but also from individual irrationality.

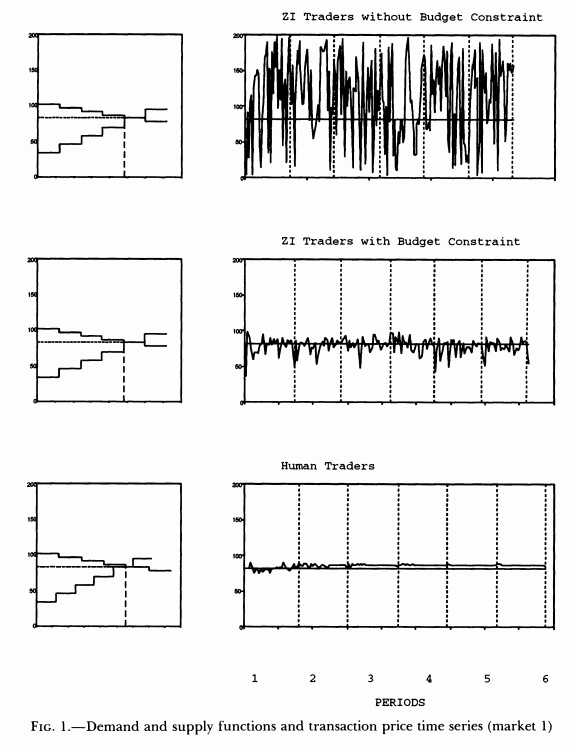

Specifically, Gode and Sunder consider two algorithms of trade. The first algorithm generates bids and asks from a uniform distribution on a fixed interval, say $[L,U]$, irrespective of the traders' reservation values. The authors refer to these traders as unconstrained zero intelligence (ZI-U) traders. In the second algorithm, bids are drawn from $U[L,v]$$\mathrm{unif}[L,v]$ and asks are drawn from $U[c,U]$$\mathrm{unif}[c,U]$, where $v,c$ are the reservation values for buyers and sellers respectively. The traders following this second algorithm are referred to as constrained zero intelligence (ZI-C) traders.

The following figure (along with several others in the paper with different market parameters) shows that ZI-U traders generate more sustained price volatility than ZI-C traders, who in turn resemble human traders in the same market condition. So I suspect that the sustained volatility you observed in your code was due to the fact that you used uniform bounds on the random bid/ask generation instead of imposing a budget constraint for the traders.