Consequently, at least when it comes to the above mentioned tenets, conventional economists reject the modern monetary theory and do not consider it useful. This is not to say that some policy recommendations might not be valid. For example, as far as I know many MMTers advocate for more government spending and higher deficits - that is not necessary bad idea especially in recession, and it is recommended policy by conventional macro models (e.g. see Mankiw Macroeconomics 8ed or Blanchard et al Macroeconomics: a European Perspective) but most conventional economists would still worry about deficits getting too out of hand and would caution against too much monetary financing (outside perhaps liquidity traps). Or most conventional economists and conventional macro models would argue it is not possible to simultaneously control inflation through taxes while simultaneously stimulating economy with monetary financed spending, in most macro models to avoid inflation you would have to raise taxes by amount exactly offsetting the effect of government spending (see Romer Advanced Macroeconomics), and to the extend government uses distortionary taxes (e.g. non-lump-sum taxes) it would leave economy worse off.

Does Modern Monetary Theory (MMT) provide a useful insight into how to manage the economy?

That depends on your definition of MMT, because it is not generally agreed on what it even is. You will find some arguing it is just a macro/monetary theory (such as the Wikipedia page) but then I seen MMT proponents on this site arguing it is a whole new paradigm that encompasses all macroeconomics and microeconomics. In addition, the MMT is not a theory in a way that is commonly understood in science, that is as far as I know there is no rigorous agreed upon MMT model that is testable. This makes it difficult to address it, because it is hard to criticize something that has no agreed upon framework as one can always simply respond to any criticism that it is not about the right interpretation of MMT.

However, this being said, the main tenets of MMT, as laid out by advocates such as Stephanie Kelton seem to include assertions that:

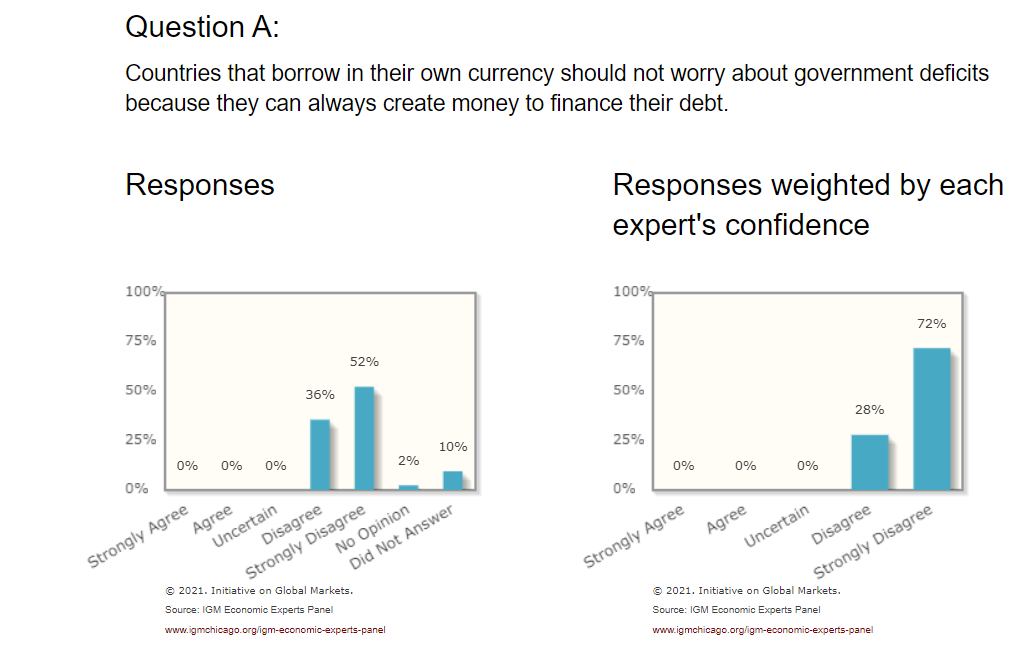

- debt and deficit for countries issuing their own currency does not matter.

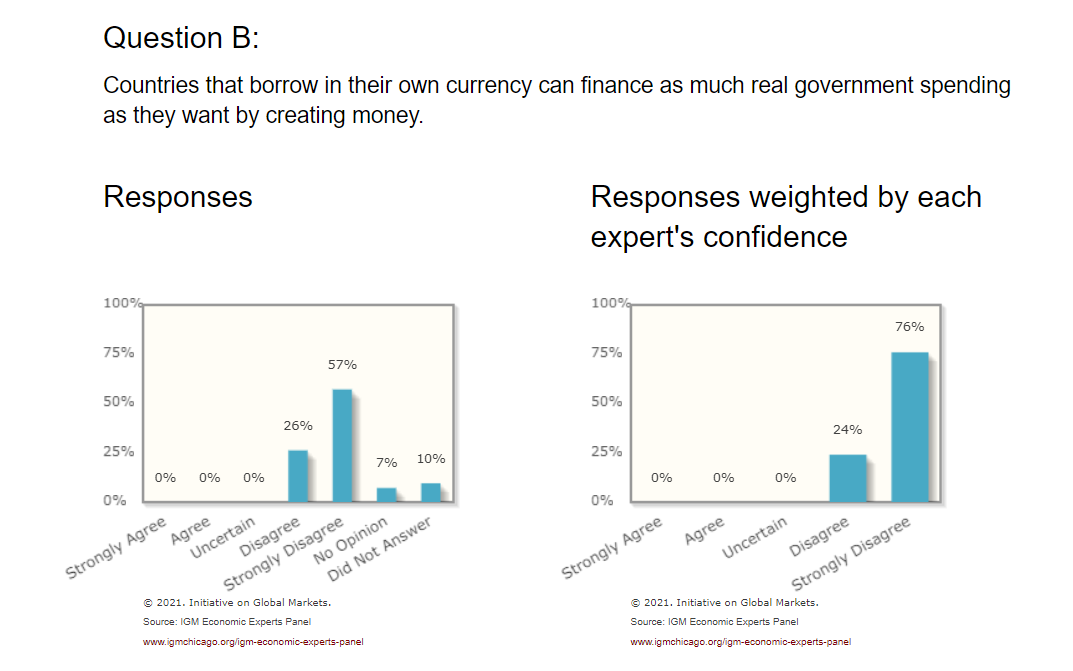

- government can fund virtually arbitrary amount of real spending through monetary financing.

This is rejected by conventional economists. In fact, an IGM poll among more than 40 top mostly Ivy league US policy economists shows that literally none of them agrees with the MMT propositions

Modern Monetary Theory

You can also have a look at critiques of MMT by other top economists such as Krugman, Rogoff, Summers or Mankiw (2019).

Consequently, at least when it comes to the above mentioned tenets, conventional economists reject the modern monetary theory and do not consider it useful. This is not to say that some policy recommendations might not be valid. For example, as far as I know many MMTers advocate for more government spending and higher deficits - that is not necessary bad idea especially in recession, and it is recommended policy by conventional macro models (e.g. see Mankiw Macroeconomics 8ed or Blanchard et al Macroeconomics: a European Perspective) but most conventional economists would still worry about deficits getting too out of hand and would caution against too much monetary financing (outside perhaps liquidity traps).

However, as stated at the beginning it is not clear what MMT is. For example, as pointed in the comments your description of MMT is quite different from what many MMT proponents asserts. For example, you state:

Government of any country with sovereign control of its own internationally accepted currency can print money to create as much inflation as it wants at will (depending on who receives that money).

But as far as I know most MMTers reject the idea that inflation is caused by expansion of money supply and rather argue inflation is consequence of different factors (such as institutional factors, or lack of competition that allows firms to hike prices and so forth). For example, according to the recently published 'MMT textbook' by the most public proponents of MMT, Mitchell, Wray, and Watts:

“Conflict theory situates the problem of inflation as being intrinsic to the power relations between workers and capital (class conflict), which are mediated by government within a capitalist system.”

Regarding your other question:

It appears to me that this must be true to some extent, but my concern is that the feedback mechanism where the extra money generates inflation might not be smooth and free flowing for various reasons and a vast excess of money might accumulate in an unstable way in certain areas of the economy. After a period of time some trigger event might cause a sudden uncontrollable cascade flood of that money that could destroy public confidence and the currency itself. Is this an unfounded fear?

This is difficult to address because it is not clear what you are trying to say here. For example, it is not clear how money could "accumulate in certain areas of the economy" (whatever that is even supposed to mean - people from selected sectors hoarding money under matrasses?) or what is meant by 'flood of money' - once money circulate they are already in the economy and have effects.

However, this being said there are many prominent economists who argue that following policies advocated by MMTers such as Kelton or Mitchell, Wray, and Watts it could lead to excessive inflation (see again the articles by the critics in previous part of the answer). There are also empirical examples of countries which attempted to excessively monetize their debt and fund spending via monetary expansion where this led to such high inflation that in the end it led to currency substitution (e.g. see Kamin & Ericsson 2003) about the Argentinian case), but I think it is more likely most developed countries would simply reverse course and change policy before going that far.