The Fisher Hypothesis is a standard example of the approach that argues that nominal magnitudes just reflect the real economy, they do not affect it. Denote $r$ the real interest rate, $i$ the nominal interest rate, and $\pi^e$ the expected inflation. Then the Fisher Hypothesis states that

$$i = r+ \pi^e$$

I write it this way to emphasize that it is the nominal interest rate that depends on the real one. In this framework, the real interest rate is determined in the real economy, say the marginal product of capital. So an increase in expected inflation will have the effect of increasing the nominal interest rate, and nothing else.

How is this rationalized?

The demand schedule for loanable funds is drawn with respect to their price. The price of loanable funds is the nominal interest rate. Magnitudes like expected inflation, if they have an effect, is to shift the whole demand schedule.

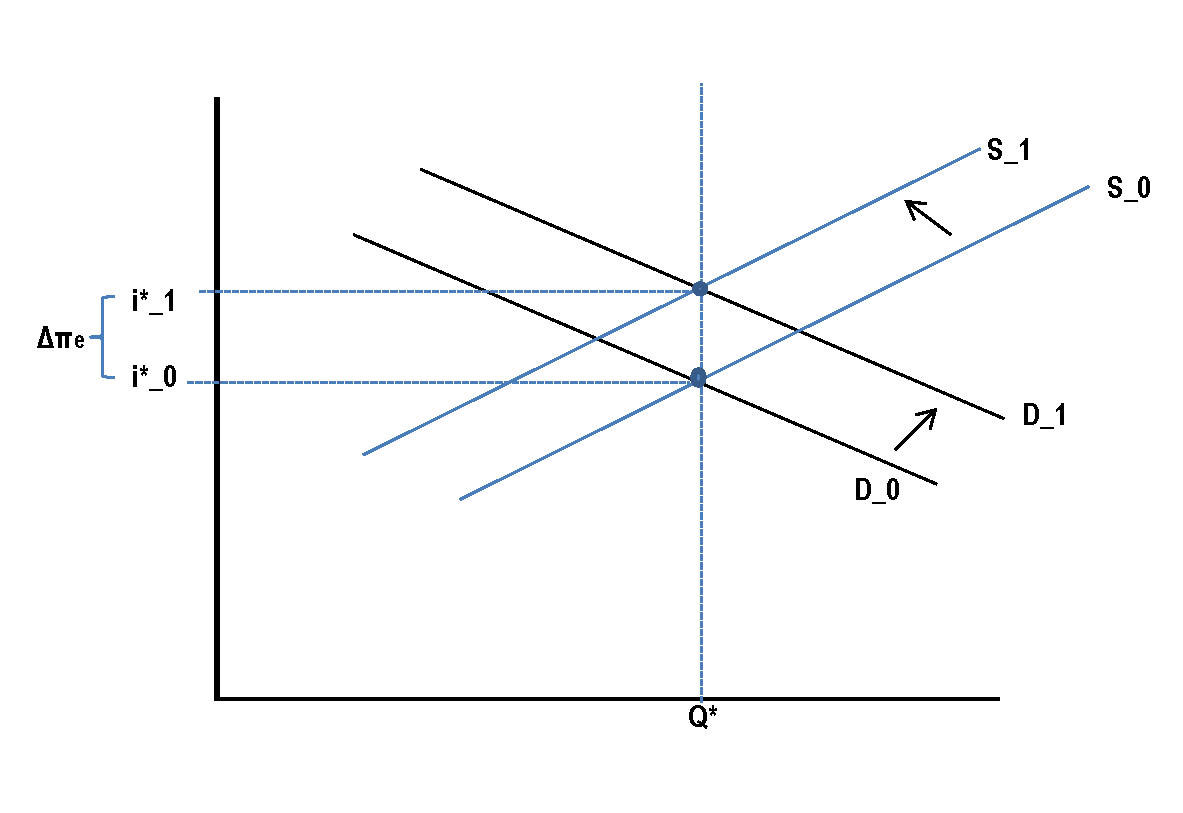

In a standard diagram, and with supply curve assumed unaffected, your answer appears strange: since when a "decrease in demand" (shift to the left of the demand schedule), leads to an increase in the equilibrium price? Intuitively, when customers start to demand less for any given price, this will lead to a lower equilibrium price, not higher. But the second part of your answer asserts that the price, i.e. the nominal interest rate, will increase due to this downward shift in the demand schedule.

Before any re-equilibrium effect, a rise in expected inflation reduces the real interest rate that prospective borrowers face. They may pay the same nominal interest rate, but the financial burden is smaller, due to the inflationary expectations: loans have just become cheaper, in real terms (while the current purchasing power they represent has not been affected).

So inflationary expectations shift the demand schedule upwards-outwards.

Now, it would be arbitrary to keep the supply schedule fixed. If expected inflation increases, prospective lenders should have a tendency to increase their current consumption, thus reducing the available funds: the supply schedule shifts upwards.

The Fisher Hypothesis says that these movements will lead to an increase in the equilibrium nominal interest rate, and the increase will be equal to the increase in expected inflation, since the real interest rate "should" remain constant.

$$\Delta i^* = \Delta \pi^e \implies \Delta r =0$$

Moreover, the equilibrium quantity of loans will be unaffected, (and so real magnitudes like consumption will be unaffected).

If no choice reflecting the above effects wherewas given to you, and if "none of the above" was not an option, then the question was deficient, or it postulated some additional assumption.