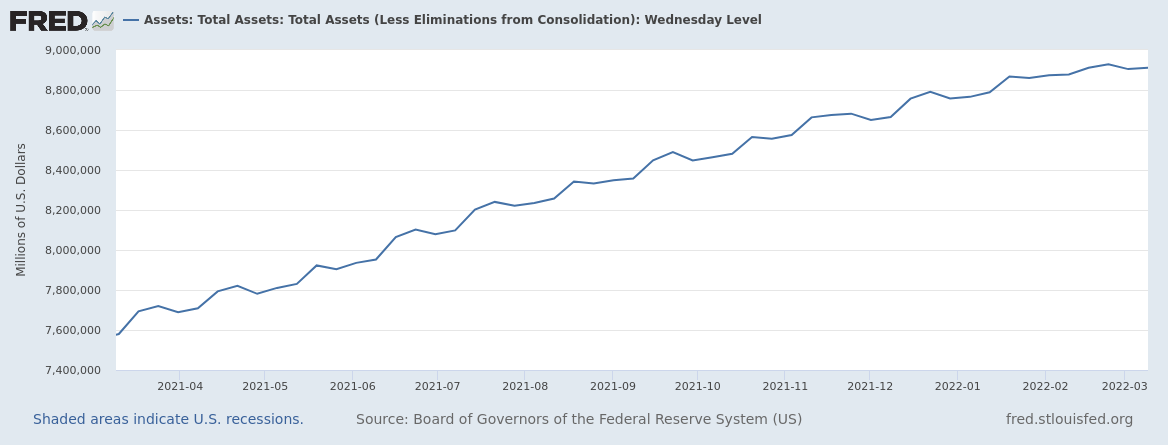

In recent months, the Federal Reserve has been purchasing bonds at a decreasing rate. This is evident in the flattening of the slope of the total assets plot.

The Fed's total assets plot...

The differential from 2022 February 23 to March 9 is close to zero. The plot has flattened recently.

Inflation was reported as 0.8% for 2022 February, which if annualized would be 10%. The one year inflation rate was reported as 7.9%. Both numbers are considered to be higher than the Fed wants them to be.

Today, 2022 March 16, the Fed is expected to announce that the short term interest rate (the federal funds rate, FFR) will be increased in order to reduce the inflation rate.

There is another way to raise interest rates. If the Fed does not purchase bonds to replace maturing bonds, the private sector would have to hold more bonds (assuming a constant level of Treasury debt, LOL) which can lead to interest rates being higher. If the Fed sells some bonds, the private sector would have to hold more bonds which can lead to interest rates being higher. Presumably some of these things can happen in the future. In 2018 and part of 2019, the Fed reduced bond holdings. This followed federal funds rate increases that started about 2 years earlier at the end of 2015. The precedent seems to be to raise the federal funds rate before reducing bond holdings.

What reasons has the Fed given in writing or the public statements of officialsin writing or the public statements of officials for increasing the federal funds rate before using balance sheet reduction (bond sales or declining to purchase to replace maturing bonds) to increase interest rates?