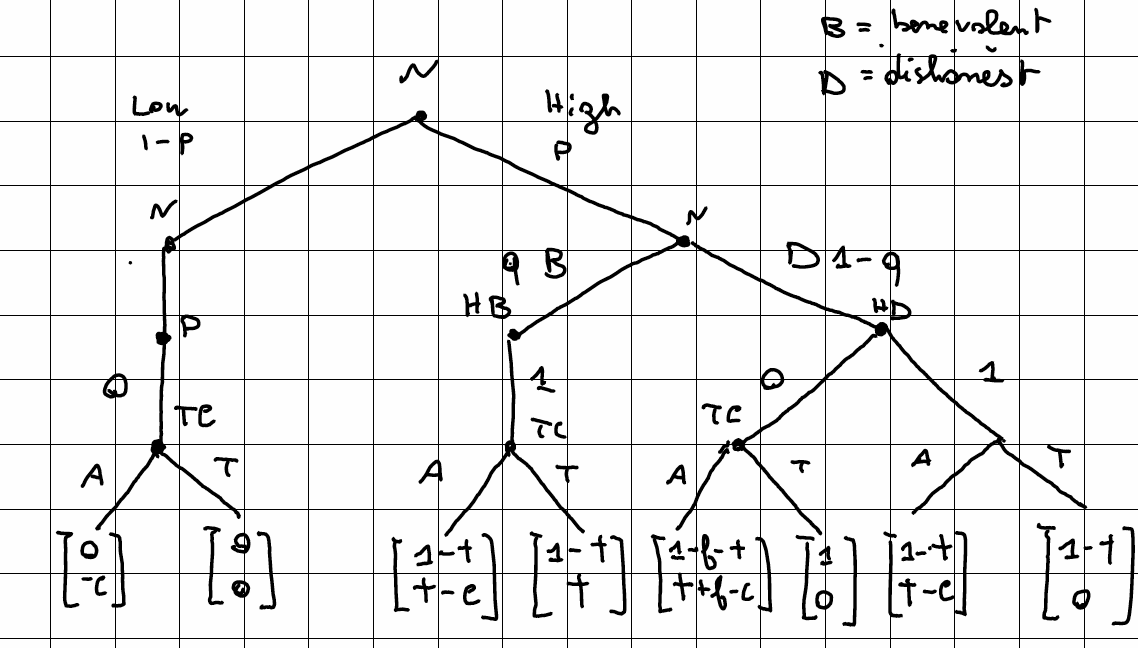

a) Without loss of generality, assume that every poor is honest. Indeed, form the perspective of the collector, the expected utility of Auditing given that someone is poor and honest or poor and dishonest is the same.

The tree takes the following form:

b) First, It's clear that everytime a rich reports 1, the tax collector won't audit. If the rich reports 0, the Bayesian belief of the tax collector that he has high income given that he reported 0 is:

$\sigma(p,q) = Pr(H|0) = \frac{Pr(0|H)Pr(H)}{Pr(0|H)Pr(H) + Pr(0|\bar H)Pr(\bar H)} = \frac{p(1-q)}{p(1-q) + 1-p}$

Hence the collector audits if and only if

$E(U(A|0)) > E(U(T|0)) \iff (t+f-c)\sigma(p,q) -c(1-\sigma(p,q)) > 0$$E(U(A|0)) > E(U(T|0)) \iff (t+f-c)\sigma(p,q) -c(1-\sigma(p,q)) \geq 0$

Thus iff $c < \sigma(p,q)(t+f)$$ \sigma(p,q) \geq c/(t+f)$, she audits when she receives a 0 report.

[The PBEa are thus $[0,-c],[1-t,t-c],[1-t,t-c]$ if $\sigma(p,q) \geq c/(t+f)$ and $[0,0],[1-t,t],[1,0]$ if $\sigma(p,q) < c/(t+f)$

c) $t+f = 1$ maximizes the tax revenue (has no economic sense, but I can't find out any mixed strategy that solves this paradox...])