This problem is an example given in Vijay Krishna's Auction Theory (2nd Edition, Chapter-6, Example 6.2). The problem is as follows:

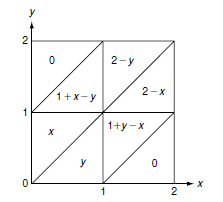

Suppose $S_1,S_2$, and $T $ are uniformly and independently distributed on $[0,1]$. There are two bidders.Bidder 1 receives the signal $X1=S1+T$,and bidder 2 receives the signal $X_2=S_2+T$. The object has a common value for both the bidders, $V=(X_1+X_2)/2$.

Now, we are required to find out the bidding strategy for a first price auction. The equilibrium bidding function is given as $\beta(x)=\int_0^xv(y,y) \,dL(y|x)$. $L(y|x)$ is further equal to $\exp(-\int_y^x\,\frac{g(t|t)}{G(t|t)}\,dt)$.

I have four questions:

- How are $X_1$ and $X_2$ affiliated?

- How is $\frac{g(t|t)}{G(t|t)}$ calculated in this example?

- How do I find the joint density of $X_1$ and $X_2$?

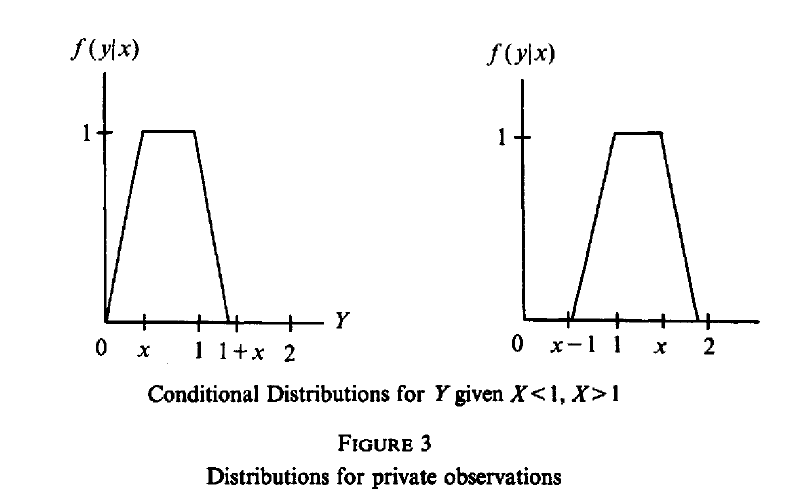

- How do I find the conditional density of $X_2$ given that $X_1=x$?