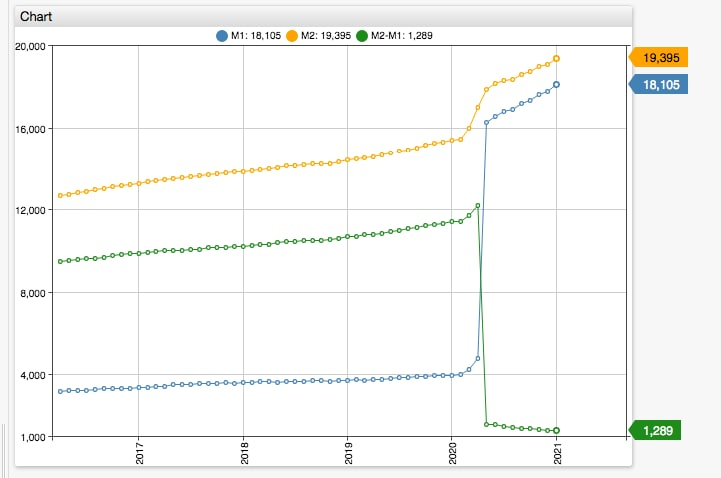

If you subtract M2SL - M1SL, the chart looks as follows:

The change is due to re-classification:

M1 before:

- (3) other checkable deposits (OCDs), consisting of negotiable order of withdrawal, or NOW, and automatic transfer service, or ATS, accounts at depository institutions, share draft accounts at credit unions, and demand deposits at thrift institutions.

M1 after:

- (3) other liquid deposits, consisting of OCDs and savings deposits (including money market deposit accounts).

M2 before:

- (1) savings deposits (including money market deposit accounts);

M2 after:

- (1) removed

Essentially savings deposits were moved from M2 to M1. Does it mean that M2 in the US now excludes all deposits regardless of term (e.g. a 10 year deposit or CD)? Is this because low interest rates reduced if not eliminated losses incurred from closing long-term deposits?