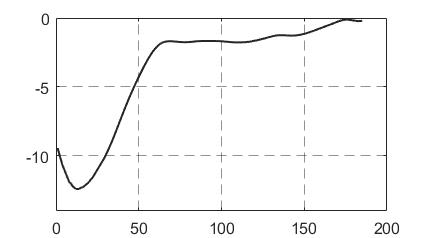

One thing to consider, is that it looks like you may have a unit root, though not necessarily.

An example of a unit root would be the stochastic process $y_k=y_{k−1}+\epsilon_{k−1}$, where the error term is mean-zero.

Unit roots can cause problems. For one, they are not stationary processes. Using OLS relies on stationarity. A violation can lead to a 'spurious regression': invalid estimates but with a high R-squared.

However, these problems are solvable. The first step is to run a unit-root test, of which there are many.

I suggest looking elsewhere for further material on this, e.g. here. There is lots out there and a full treatment would be outside the scope of one answer.