Explicit Reasoning

This post is edited substantially in the hope of clarifying how credit flows increase, decrease, or do not increase or decrease the levels taken to be the statistical measures of the elastic money supply in the depository institutions.

The Financial Accounts Guide All Tables

https://www.federalreserve.gov/apps/fof/FOFTables.aspx

Scrolling down one observes financial statistics tables organized as Sectors: Transactions (links in the left side column) and Sectors: Levels (links in the right side column).

Transactions in these financial tables are classified as economic flows. These are financial flows caused by credit/debt deals.

Levels in these financial tables are economic stocks. The creditors own financial assets and the debtors owe liabilities or debts to the creditors. The flows of credit/debt deals increase or decrease the stocks of financial assets and liabilities because the financial tables are designed to be stock-flow consistent in accord with legal interpretations of credit/debt instruments and accounting customs for recording financial assets with matching liabilities.

Four Sector Model

| Sovereign |

All Other |

|

| Fed |

Banks |

Money Generators |

| Treasury |

Nonbanks |

Money Users |

Sovereign sector consists of the monetary authority (Fed) and the Treasury branch of the central government. Money supply is mostly generated by the Fed and Bank sectors of the economy which respectively issue base money and bank money as liabilities on the respective balance sheet.

If the Treasury branch sells government securities to cover the deficit spent for a period, and if Treasury net redeems government securities to dispose of a surplus for a period, then the Treasury operates like a Nonbank Money User. The purpose of this activity in the United States is to neither add nor remove bank reserves via the deficit/surplus. This helps the Fed retain control over monetary policy by using its balance sheet to add or remove bank reserves in the aggregate Bank sector when necessary.

Nonbanks include any unit that is not classified as either Sovereign or in the Depository Institution sector (Banks). Some economic papers refer to Nonbank financial firms as banks because they provide credit to hold a financial asset portfolio and issue a mix of debt and equity to hold the financial assets, just like banks, but these Nonbank firms do not increase or decrease the money supply by entries on their balance sheets (except for the inclusion of retail money market mutual funds in the definition of M2 money supply).

Money Users clear payments by the transfer of ownership claims to liabilities of the Bank sector, and Nonbanks make credit deals among each other, but these transaction mechanisms do not change levels in the money supply because Banks are not direct counter-parties when clearing payments.

Money Stock Measures

https://www.federalreserve.gov/releases/h6/current/default.htm

Base Money

| Base Money |

Issuer |

| Reserve Balances |

Fed |

| Vault Cash |

Fed |

| Currency outside Fed, Treasury, Banks |

Fed |

M2 Money Stock

Simplified model for M2 money stock defined as of May 2020. M2 includes components of M1 shown as M1/M2.

| Component |

Issuer |

Notes |

| Currency |

Fed |

M1/M2 Currency held by Nonbanks |

| Checkable Deposits |

Banks |

M1/M2 deposits held by Nonbanks |

| Other Checkable Deposits |

Banks (Thrifts) |

M1/M2 liquid funds held by Nonbanks |

| Savings Accounts |

Banks |

M1/M2 savings accounts held by Nonbanks |

| Small Time Deposits |

Banks |

M2 time deposits held by Nonbanks |

| Retail Money Market |

Nonbanks |

M2 money market funds |

Levels of Monetary Authority (Fed)

https://www.federalreserve.gov/apps/FOF/Guide/L109.pdf

Note three liabilities of the Fed are counted in the base money supply or monetary base also known as MB or M0:

Depository institution reserves

Vault cash of depository institutions

Currency outside banks

Currency Drain and Fed Securities Holdings

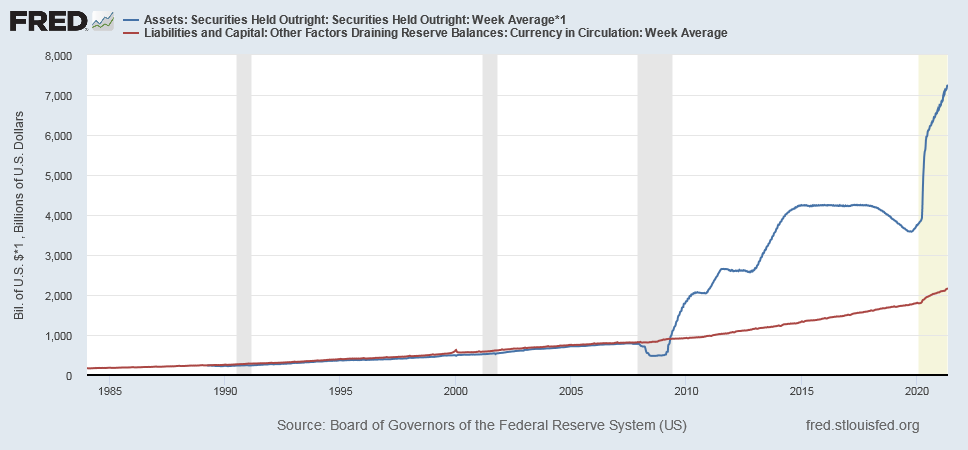

Prior to the financial crisis of late 2008 Fed buys securities in the open market which are roughly equal to the level of its currency liabilities. This means the Nonbank sector has the option of holding securities, which earn interest, or currency, which earns no interest, because Fed would do an asset swap with the Nonbank sector to satisfy its demand for currency versus other financial assets. Prior to late 2008 Fed would purchase primarily Treasury securities and other Agency debt issued by or guaranteed by the federal government. After 2008 Fed began large scale asset purchases and paid interest on excess reserves created via LSAP open market operations. Before 2008 Fed would service the currency drain to ensure banks did not become depleted of reserve balances and vault cash due to the net withdrawal of currency over time.

FRB H.4.1 Release shows Factors Supplying Reserve Balances including Reserve Bank credit and other assets listed on the Fed balance sheet:

https://www.federalreserve.gov/releases/h41/current/

FRB H.4.1 Release also shows Total factors, other than reserve balances, absorbing reserve funds including currency in circulation and all Fed liabilities other than reserve balances.

So Fed manages the level of reserve balances by using Reserve Bank credit to supply reserve balances when necessary if other factors absorb reserve balances. Some items on the balance sheet are autonomous, or not under the control of Fed, and other items are control factors such as levels of Reserve Bank credit. The flow of Reserve Bank credit is used as a control factor to supply levels of reserve balances against factors absorbing reserve balances as necessary to support the monetary policy goals of the Monetary Authority.

Simplified Bank Balance Sheet and Income Statement

Loan Loss Reserve Accounting and Bank Behavior (4 pages)

https://www.richmondfed.org/~/media/richmondfedorg/publications/research/economic_brief/2012/pdf/eb_12-03.pdf

Levels of Private Depository Institutions

https://www.federalreserve.gov/apps/FOF/Guide/L110.pdf

Currently the first three lines are Total financial assets, Vault cash, and Reserves at Federal Reserve. Assume non-financial assets are negligible compared to the magnitude of financial assets. Then define Bank Credit:

Bank Credit = Total financial assets - Vault cash - Reserve balances

Bank assets are classified broadly as either Bank Credit or Total Reserves. In the paper above "Cash" would correspond to and contribute to "Total Reserves" of the Depository Institution sector. Bank Credit would include Loans and all other financial assets held by each bank but would specifically exclude reserves. The bank sector uses reserve balances at the central bank to clear interbank payments and uses vault cash to service withdrawals of currency from the bank.

This graph shows that US Bank Credit grows historically without a corresponding increase in Total Reserves prior to the US financial crisis of 2007-2008:

One may infer that the Bank sector, also known as Depository Institutions sector, does not require a net increase in total reserves to expand Bank Credit at least over the period shown prior to the 2007-2008 crisis. Then the question is how the depository institutions expand bank credit without a significant increase in total reserves?

Simplified Chart of Accounts for the aggregate Bank sector (Depository Institution) balance sheet.

| Assets |

Liabilities |

| Reserve Balances |

M1/M2 deposits held by Nonbanks |

| Vault Cash |

Money market borrowing from Nonbanks |

| Securities |

Borrowing from Fed at discount window |

| Loans |

Equity |

| Other |

|

Accounting rules specify that Assets increase by a debit entry and liabilities or equity increase by a credit entry; also Assets decrease by a credit entry and liabilities or equity decrease by a debit entry. Transactions in the aggregate bank sector may or may not increase or decrease components of M1/M2 money depending on which accounts in the Chart of Accounts get debit and credit entries.

Reasoning by analogy to the Monetary Authority balance sheet, which gives the factors supplying reserve balances and the factors absorbing reserve balances, the Depository institutions balance sheet would have factors supplying M2 deposits and factors absorbing M2 deposits. We can write these factors in an identity as follows:

M1/M2 Deposits = Reserve Balances + Vault Cash + Bank Credit - Liabilities* - Equity

where a transaction in the aggregate bank sector can increase, decrease, or neither increase nor decrease M2 deposit levels due to double-entry accounting customs. Liabilities* include components of Bank liabilities that are not counted in aggregate measures of the M2 money supply.

Fed generates net new reserve balances and M1/M2 deposits when it purchases securities from Nonbanks. The aggregate Bank debits reserve balances for an increase and credits M1/M2 deposits held by the Nonbank sector for an increase to clear payment between Fed and Nonbank units. Before late 2008 Fed used these open market operations to offset the currency drain (withdrawal of currency) from the Bank sector and to provide banks with just enough reserve balances so a few banks would show up at the discount window to borrow overnight funds. By monitoring the discount window activity Fed has information about the efficiency of the fed funds market and by keeping the aggregate Bank sector a little short on reserve balances Fed can control the fed funds interest rate.

After late 2008 money markets were seriously disrupted, discount window borrowing went up significantly, and initially Fed sold Treasuries from its balance sheet to "sterilize" the increase of reserves provided at the discount window. However this strategy would deplete Fed of its best asset class, Treasury securities, if the aggregate Bank sector kept demanding more reserve balances via borrowing from Fed. So Fed went to Congress for authority to pay interest on excess reserves and switched to providing excess reserves via large scale asset purchases (LSAP) in late 2008 into early 2009. If Fed does LSAP purchase with Nonbanks then Banks would debit reserve balances for an increase and M1/M2 deposits for an increase caused by the increase of Fed Credit.

Fed generates net new reserve balances when it purchases securities from a Bank or makes discount window loans to a Bank. Banks do not debit or credit M1/M2 deposits when dealing directly with Fed so there is no change in M1/M2 money for these transactions. When Fed purchase securities, either from a Bank or Nonbank, this provides so-called "non-borrowed reserves". When Fed lends to Banks this provides so-called "borrowed reserves."

Nonbanks decrease vault cash and M1/M2 deposits via the long term withdrawal of currency from the aggregate bank. Banks pay for vault cash using reserve balances at Fed. So the long term currency drain would deplete banks of vault cash and reserve balances if Fed fails to service the currency drain (buy securities equal to or slightly greater than its currency liabilities) before late 2008. After late 2008 Fed provides excess reserves via LSAP and no longer needs to service the currency drain as shown in the graph above of securities held compared to currency liabilities.