First, lets be clear - I'm not pitching a crypto here, and I'm not seriously interested in Safemoon, which seems to be a pyramid scheme.

However, I was investigated Safemoon, and discovered this concept of liquidity pools and decentralised exchanges.

You can see a video here explaining how the LP works.

A liquidity pool is basically a mechanism to price and exchange two commodities, without having a third party manage an order book - like a conventional stock exchange does.

Constant Product Equation

Basically the a LP is created with two different tokens, A and B.

The constant product equation is :

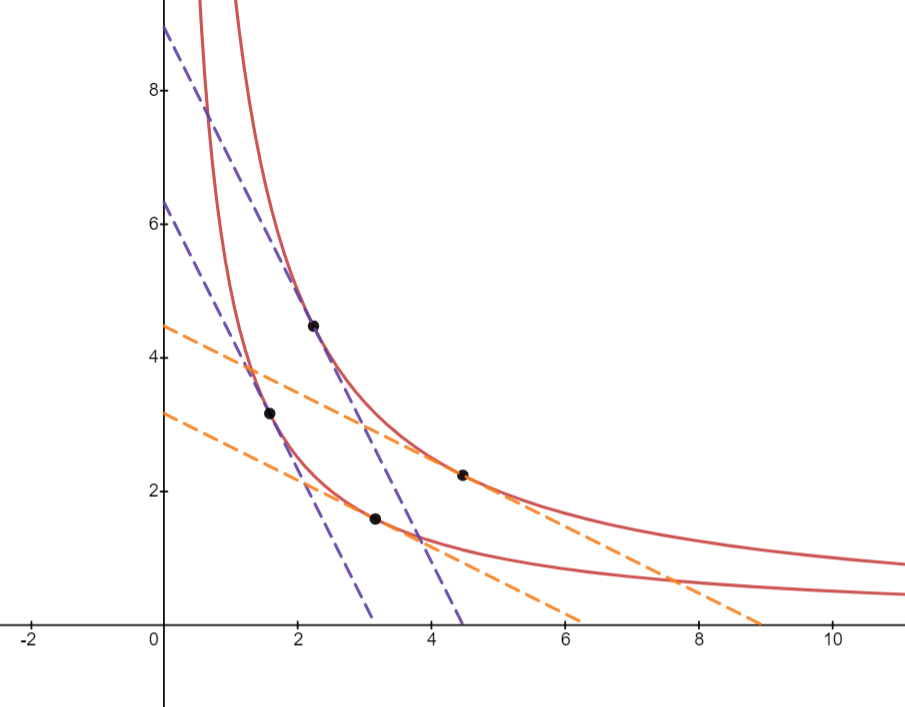

K = A * B

As an example:

Say I have I create a LP with 1000 A and 100 B then K = 100,000.

Now someone deposits 100 B into the LP, then in order to keep K constant they will receive 500 A to keep K constant. (500 * 200 = 100,000).

But now if someone deposits another 100 B, they would receive only 167 A (333 * 300 = 100,000).

As the video points out, this causes the price to asymptote as you head towards either extreme of imbalance of the coins, and the video bills this as a good thing.

How good is this system really?

The idea of an algorithmic system, that doesn't require a third party to exchange, I can see the appeal.

To take a real world scenario, you have people with bags of rice, and people with dollars. You could determine the price per bag using an order book.

I wondering if using a liquidity pool just as effectively prices the goods.

My initial thought is that it seems that the initial values of A and B very much 'stick' the price to within a certain band, and the price doesn't have much flexibility in moving beyond there.

I will note that Safemoon does have a mechanism that increases the K value, and that's a whole thing, so I think if the answer is 'Yes the ratio of A:B and the K value generally informs the price, and to move the price you need to adjust the K value, then it becomes a question of 'who/what determines the new ratio and K value?'.