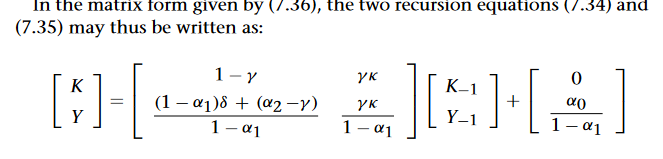

Good evening everyone ! I'm currently reading Godley and Lavoie Monetary economics. It's really an awesome book, and I'm at the 7th chapter where they introduce private bank money. The model is very simple, but I'm struggling to derive simulations on the short-run. I use the following equations given by the author:

\begin{gather*} Y\ =\ C\ +\ I\\ Amortisation\ =\ \delta K_{-1}\\ WB\ =\ Y-r_{-1} L_{-1} -\delta K_{-1}\\ \Delta L=I-Amortisation\\ YD\ =\ WB\ +\ r_{-1} M_{-1}\\ C\ =\ a_{1} YD\ +\ a_{2} M_{-1}\\ K\ =\ K_{-1} \ +\ ( I-\delta K_{-1})\\ K^{T} \ =\ kY_{-1}\\ I\ =\ y\left( K^{T} -K_{-1}\right) +\delta K_{-1} \end{gather*}

Where:

\begin{gather*} Y\ =\ total\ output\\ YD\ =\ available\ income\\ WB\ =\ wages\\ L\ =\ total\ loans\\ M\ =\ savings\\ C\ =\ consumption\\ K\ =\ capital\\ K^{T} \ =\ targeted\ capital\\ I\ =\ investment \end{gather*}

Like you can see, there's two main problems with the equation presentation: (1) there's function with time (I think that's a problem through the book, even if the authors use time graph), (2) the link between output, wages, and capital accumulation is not explicit. In accordance with those problems, I have the following questions:

A. How can I built a model estimating output and available income through time from the previous equations?

B. How do Godley and Lavoie modelize (on the short-run) the dynamic relation between capital accumation, output, and wage?

C. Is there any SFC consistent model integrating time explicitly (in the equations) - the equations from Godley-Lavoie are killing me because there's no explicit modelisation with time?