In most first-year undergrad macroeconomics courses, students are taught about the Phillips curve and how whilst there may exist a tradeoff between inflation and unemployment in the short-run, there is no such thing in the long-run as a result of agents adjusting inflation expectations. Is this result valid or could it be the case that the natural rate of unemployment changes with the output gap, in which case there could exist a long-run trade-off between inflation and unemployment?

Add a comment

|

2 Answers

$\begingroup$

$\endgroup$

$\endgroup$

2

could exist a long-run trade-off between inflation and unemployment?

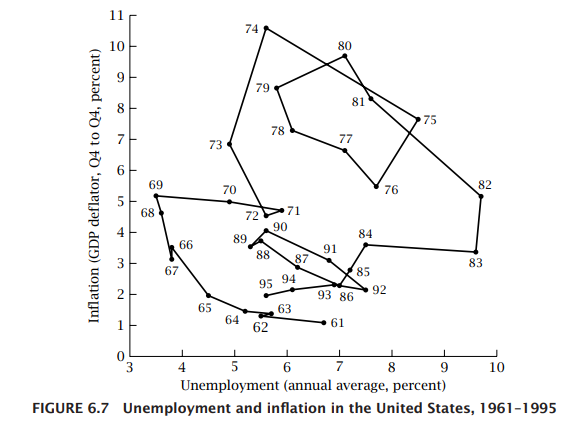

This depends on the long-run shape of Philips curve. Well done and highly cited empirical studies generally cannot reject the long run Philips curve is flat implying there is no long run inflation unemployment trade-off, although alternative explanation is that current studies are simply not powered enough to detect (very) small slope of long run Phillips curve.

Following Benati 2015:

Both cointegration methods, and non-cointegrated structural VARs identified based on either long-run restrictions, or a combination of long-run and sign restrictions, are used in order to explore the long-run trade-off between inflation and the unemployment rate in the post-WWII U.S., U.K., Euro area, Canada, and Australia. Overall, neither approach produces clear evidence of a non-vertical trade-off. The extent of uncertainty surrounding the estimates is however substantial, thus implying that a researcher holding alternative priors about what a reasonable slope of the long-run trade-off might be will likely not see her views falsified.

....

Overall, the evidence discussed in this paper provides essentially no support to the notion of a non-vertical long-run Phillips trade-off—in particular of a trade-off which can be actively exploited by a policymaker in order to permanently reduced the unemployment rate.

In addition you can also see from data that there does not seem to be any long-run relationship (see ibid pp 258).

PS: One should not confuse hysteresis effect (situation where temporary shocks have permanent effect), with Phillips curve inflation-unemployment trade-off where increase in inflation can decrease unemployment and vice versa.

Let me illustrate the difference.

Inflation Unemployment Trade-off

Suppose that the Phillips curve is given by following equation (see Romer Advanced Macroeconomics pp 259):

$$\pi = \pi^* + \beta (y_A- \bar{y}_A) + e$$

where $\pi$ is inflation $\pi^*$ expected inflation and $y$ is a log of actual output and $\bar{y}$ log of natural level output so the expression in brackets is output gap. Output gap in turn determines the level of employment in the economy.

Now in short run there will be a inflation/unemployment trade-off (non-flat Phillips curve) as long as $\pi \neq \pi^*$ (since $\pi \neq \pi^*$ implies inflation can affect output and thus employment which correlates with output). However, suppose that in long run $\pi = \pi^*$. In that case we will have no inflation employment trade-off.

Hysteresis

Now suppose we have not just one equation but 2

$$\pi = \pi^* + \beta (y_A- \bar{y}_A) + e \tag{1}$$

and

$$\pi = \pi^* + \beta (y_B- \bar{y}_B) + e \tag{2}$$

where $(y_B- \bar{y}_B)< (y_A- \bar{y}_A)$, with a switching rule that we move from equation (1) to (2), whenever output gap $(y_A- \bar{y}_A)$ passes some threshold for triggering hysteresis $k$.

Clearly as long as we assume that $\pi= \pi^*$ in long run Philips curve is flat (no employment inflation trade-off) in spite of the hysteresis effect.

answered Mar 11, 2022 at 15:27

-

$\begingroup$ As outlined in a comment to my answer, you are confusing the gap measure $y-\bar y$ with actual unemployment. The fact that a large enough output gap $y_A-{\bar y}_A$ moves you from ${\bar y}_A$ to ${\bar y}_B$ for $\pi=\pi^*$ in the long-run implies a tradeoff between inflation today and output/employment. Put differently, you are arguing with two different PCs, neither of which contains the measure we are actually interested in. $\endgroup$– jpfeiferCommented Mar 11, 2022 at 15:33

-

$\begingroup$ @jpfeifer 1. employment is correlated with output $y$, higher output means higher employment. It is normal in macro literature to talk in terms of output gap. However, I edited the answer to make it more clear. 2. But inflation employment tradeoff does not mean that inflation can have just one time effect on employment. Inflation employment tradeoff means that employment is some inverse function of inflation. In the hysteresis model it simply isn’t. Hysteresis is tantamount to structural beak in relationship. $\endgroup$– 1muflon1 ♦Commented Mar 11, 2022 at 16:19

$\begingroup$

$\endgroup$

9

Opinions differ (as always in economics) but there is some evidence that there also a long-run tradeoff due to hysteresis. Long periods of unemployment may cause the natural rate of unemployment to move up as well, e.g. due to the loss of human capital or insider-outsider dynamics in labor markets. One of the earliest papers is the Blanchard/Summers (1986) paper. But already Phelps (1972) in his book outlined that hysteresis may cause the long-run Phillips curve not to be vertical. See for example Cross (1987)

Studies like Di Bella et al. (2018) suggest this to also be an empirical issue. Hysteresis implies that for example fully stabilizing inflation at a low level vie monetary policy after temporary supply shocks may result in permanently higher unemployment. This contrasts with typical Phillips curve models where the natural rate of unemployment is independent of such demand factors like monetary policy.

-

$\begingroup$ Hysteresis effect on unemployment is not the same as long run trade off between inflation and unemployment. Hysteresis in unemployment would be a long run effect of not taking action in a short run. Hysteresis essentially kicks the economy into “worse” equilibrium. That is fundamentally different mechanism from there being long run trade off between inflation and unemployment $\endgroup$– 1muflon1 ♦Commented Mar 11, 2022 at 14:12

-

$\begingroup$ I am not sure I am following. Hysteresis will typically imply that shocks that have an effect on today's inflation (and relatedly the output gap) will also have an effect on long-run unemployment. The OP asked about a relation where the "the natural rate of unemployment is positively related to the output gap". I would argue that is the case if there is hysteresis. $\endgroup$– jpfeiferCommented Mar 11, 2022 at 14:18

-

$\begingroup$ I dont think the OP fully knows what he is talking about but the question in title and last sentence say "could exist a long-run trade-off between inflation and unemployment?" If there is a long run tradeoff between inflation and unemployment the Phillips curve cannot be horizontal in long run. There always needs to be trade off. Hysteresis represents change in long run equilibrium. For example suppose long run equilibrium unemployment is 4% and Philips curve is completely flat. A sufficiently large negative shock can permanently knock the long run unemployment to 8% but that does not mean $\endgroup$– 1muflon1 ♦Commented Mar 11, 2022 at 14:51

-

$\begingroup$ there is any long run relationship between inflation and unemployment. Once you are in the "bad equilibrium" Philips curve will be flat. It is true that in a short run you could prevent hysteresis from occurring by maybe some more aggressive inflationary policy saying that is fair, but that does not mean that in a long run unemployment responds to change in inflation (i.e. you have completely flat phillips curve in long run). $\endgroup$– 1muflon1 ♦Commented Mar 11, 2022 at 14:54

-

$\begingroup$ I think your interpretation is wrong. You are correct that the long-run PC in hysteresis models is flat, but in the unemployment gap. That does not make it flat in the actual unemployment rate if the NAIRU is changing due to hysteresis. Put differently, the tradeoff is reflected in the intersect, not the slope if you consider the typical variables on the axes. You may want to have a look at Cross 1987, page 87. $\endgroup$– jpfeiferCommented Mar 11, 2022 at 15:20