As someone coming from a mathematical background who has started reading into some basic finance, there are a few concepts that I am struggling to understand and would be grateful if I could check to see whether or not my understanding of these is correct.

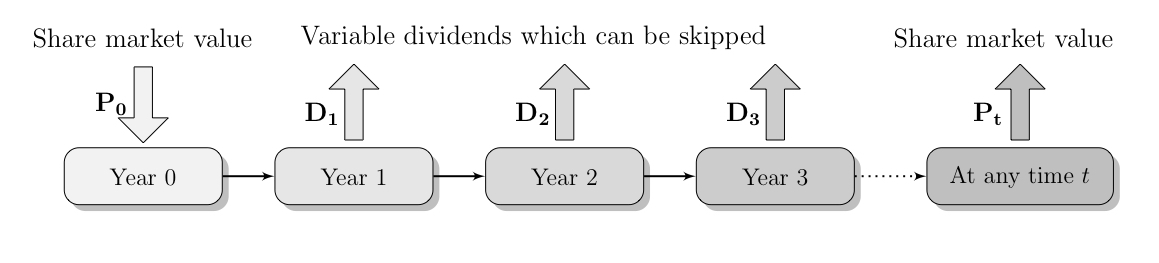

The first concerns the distinction between ordinary and preference shares. I understand the theoretical difference between the two, but I am confused about what this diagram for ordinary shares means

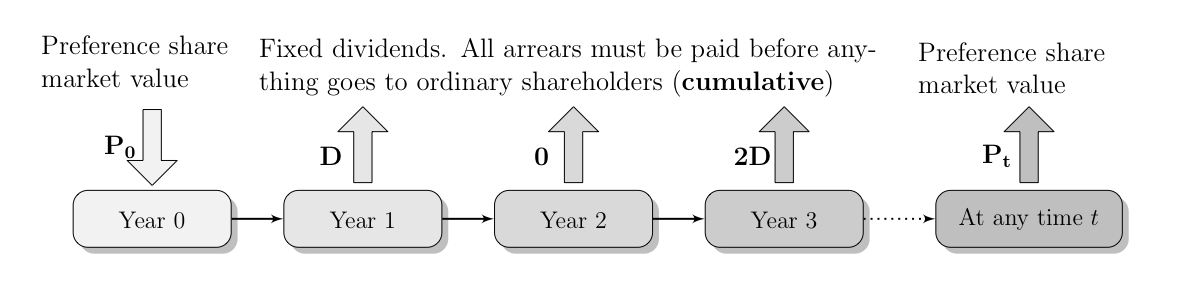

And similarly, there is also a diagram for preference shares:

My guess is that (based on the above diagrams), this seems to suggest the following result:

$P_t = P_0 - \sum_{i=1}^{t-1} D_i$ for ordinary shares

As for Preference Shares, I am quite confused as to what the relationship is here between $P_t$ and $P_0$. The removal of $D$, then $0$, then $2D$ doesn’t seem to display a clear pattern and so I’m not entirely sure what this diagram illustrates here.

The text gives no numerical examples (as it is more focussed on the theoretical side), however, I’m interested in what the mathematical relationship is between these quantities and what these diagrams are trying to show.