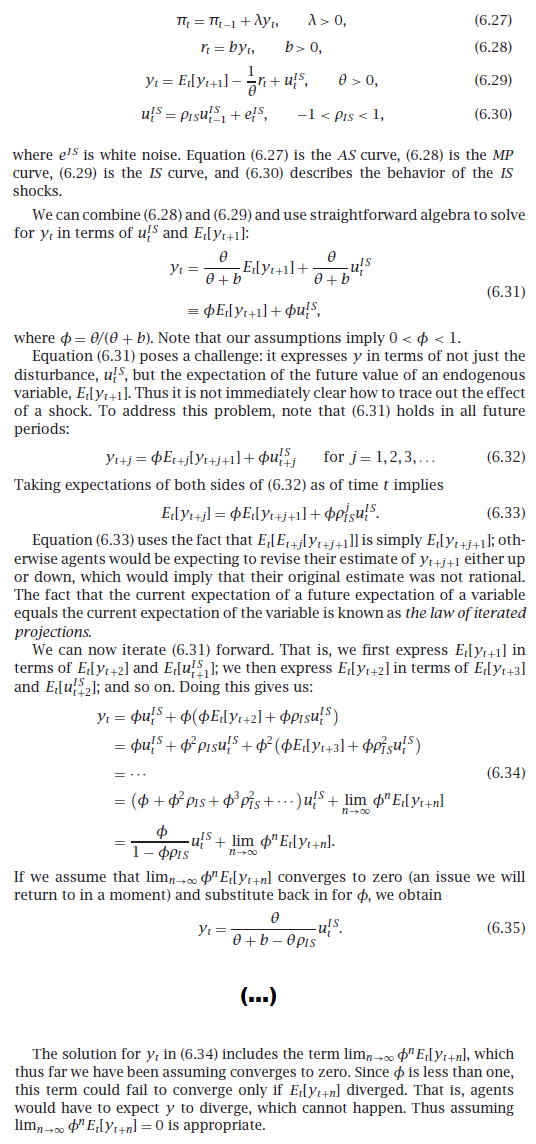

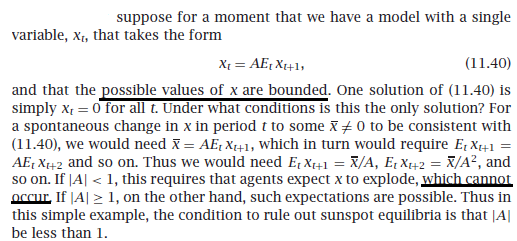

QUESTION 1

By inserting $(6.28)$ into $(6.29)$, re-arranging and applying direct forward substitution , we obtain

$$y_t = \lim_{n\rightarrow \infty}\left[\left(\frac {\theta}{\theta + b}\right)^nE_t[y_{t+n}]\right] +\frac {\theta}{\theta+b -\theta \rho}u_t \tag{1}$$

Then forwarding $n$ periods and taking the conditional expectation with respect to information available at $t$ we have

$$E_t[y_{t+n}] = E_t\left(\lim_{n\rightarrow \infty}\left[\left(\frac {\theta}{\theta + b}\right)^nE_{t+n}[y_{t+2n}]\right]\right) +E_{t}\left(\frac {\theta}{\theta+b -\theta \rho}u_{t+n} \right)$$

$$\implies E_t[y_{t+n}] = E_t\left(\lim_{n\rightarrow \infty}\left[\left(\frac {\theta}{\theta + b}\right)^nE_{t+n}[y_{t+2n}]\right]\right) \tag{2}$$

The conditional expectation is an integral. Can we interchange integration and limit? To do that Dominated Convergence & Co should hold (they are only sufficient conditions, but we do not have something better). For our case, Dominated Convergence requires that the expression inside the limit is bounded("dominated"), and that the limit is finite. If it is then, using also the Law of Iterated Expectations, and the fact that under the limit $t+2n$ is equivalent to $t+n$ we have

$$E_t[y_{t+n}] = \lim_{n\rightarrow \infty}\left[\left(\frac {\theta}{\theta + b}\right)^nE_t[y_{t+n}]\right] \tag{3}$$

Note carefully that in the left-hand side, $n$ does not go to infinity. Also, remember that we obtained $(3)$ under the assumption that the limit is finite. So $(3)$ tells us that for every finite $n$, the conditional expectation must be equal to the unique limit, i.e. equal to the same number, i.e. it should be a constant.

Can this constant be anything else than zero? Assume the limit is not zero. Then one can verify that the only other finite value that the limit can take is $1$. But for the limit to be $1$ we must have

$E_t[y_{t+n}]\rightarrow \left(\frac {\theta + b}{\theta}\right)^n$, which goes to infinity with $n$. So the left hand side would go to infinity and will not be equal to the limit. Hence we conclude that the limit must be zero, for $(3)$ to hold.

This can happen if we assume that the expectation alone is a non-zero constant, or that it is growing but boundedly (say, it has an asymptote to which it converges from below). But then again, in both cases the left hand side will not be equal to the now zero limit. So we see that the only way that $(3)$ can hold is to assume that the expectation alone is zero.

So I would say that the approach "if we assume that the limit is zero, then we obtain etc" (as presented in the quoted text), is wrong: looking at our solution, which is equation $(1)$, we must first assume/impose that the expectation is zero, to make it all consistent, and finite (note: if the solution $(1)$ included also a constant term in the right-hand side, things would be more flexible).

Sticking with $(1)$, we also see that the only other consistent solution is to assume that the limit goes to infinity -and this can happen only if we assume that the expectation on its own goes to infinity.

QUESTIONS 2 & 3

As I have wrote in another answer, everything in real-world economics is finite -even prices, even expectations. The above mathematical formulations and the mathematical possibility of an infinite solution represent in a colorful way the phenomenon of "bubbles". In real life, bubbles eventually burst -but what we have managed to capture by using the "infinity" concept, is the abnormal inflation of the bubble while it hasn't burst yet. So agents can "expect infinity", in the metaphorical sense just described. But since "bubbles" is not your everyday economic phenomenon, these models usually assume them away in order to study the stable situation.

Marx was the one that argued that capitalism will explode, or rather, implode. So you have an articulated theory that advances the view that a specific economic system possesses the property of (eventual) divergence.