I have the following inter temporal utility function:

$U(t)=(\frac{s(t)}{1-\sigma})(c_t/c_{t-1}^\gamma)^{(1-\sigma)} - \chi*h(t)$

where $h(t)$ is the hours worked.

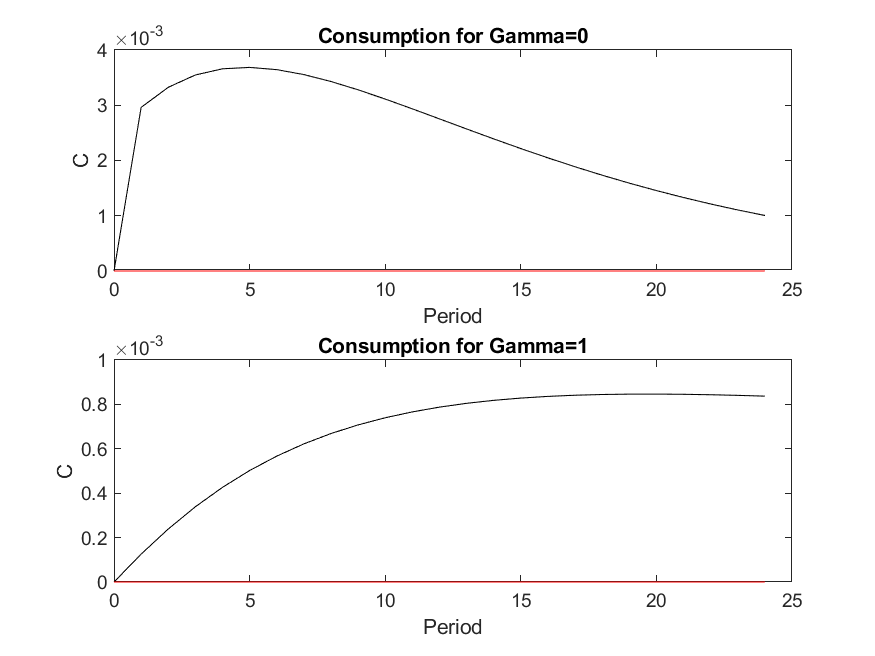

I know that gamma is responsible for consumption smoothing as I have achieved the following results after a positive shock on $s(t)$:

The problem is i do not know how to prove mathematically that when gamma=1 consumption is smoother