I assume that this is about Macroeconomics in particular (you might want to add that tag).

Often we don't need profits

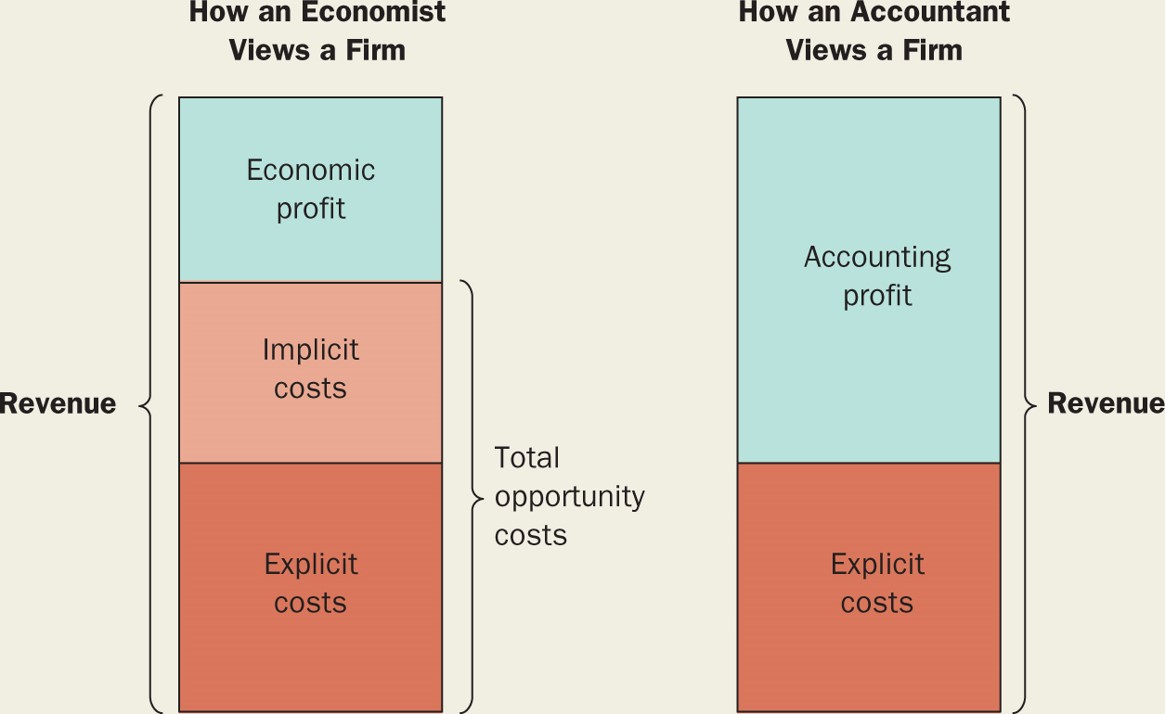

The interaction of firm profits is often irrelevant. It is well summarized under capital rents. Having firm profits does not add any insights to, say, Solow's growth model or the standard Neoclassical model.

Operative profits vs Life time profits

In some models, however, we do need profitability of firms. That typically comes from additional costs of running the firm. For example

- Vacancy costs (search and matching model)

- Entry costs (patents in Romer's growth model)

Firms run positive operative profits, which exactly offset the entrance costs. That is, life time profits are zero.

Why? Because we start in many models from the first-best and gradually remove particular assumptions. Romer could have talked in his model about a world in which patents have limited enforceability, or competitors particularly catch up, but the standard models we research ( and teach) typically do not incorporate this.

Later on, Kortum (1997) and Aghion, Howard, Howit create research based growth models that allow for catching up of competitors.

Profits are messy to model

Profits mess up a lot of things. Think about the neo keynesian model, a standard example of where firms make profits (positive or negative) in every period, which do not necessarily cancel out over time. Allow for heterogeneity in households assets: some are poor, some are rich.

Perfect representation of the owner in the decision making process of the firm requires that the stochastic discount factor (SDF) of the firm represents the SDF of the owner. But, in this model, who is the owner? Rich and poor agents share the firm, with different degree of ownership. To do this properly, we would need to add a stock market for the firm and allow agents to trade it; track the ownership of the firm and adjust the SDF.

But no, you can't even look at the share of ownership: Say, $w$ denotes the wealth level, $m(w)$ denotes the measure of firm assets hold by agents with wealth $w$, and $\rho(w)$ denotes the discount rate of agents with wealth level $w$. Can you then just compute the firms SDF $\rho_F$ with

$$\rho_F = \int \rho(w)m(w) dw$$?

In reality, firm decisions are often voted over by simple majority. You'd need to model coalitions that get votes of $50%$ of asset holdings and see what SDF that gives you.

Of course, this is much too complicated to do correctly. Even the intermediate step with an asset market is not trivial, people very often fall back to assuming the SDF of the richest agents, predicting their model's outcome. But it's not nice: We like to have internality consistent models, and profits make this difficult.