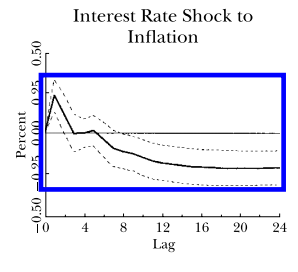

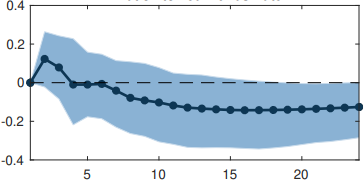

Typically in statistical software, the default confidence level is 95%. The higher the better, I suppose. But this is still not a rule of thumb, right? In Stock and Watson's paper (https://www.aeaweb.org/articles/pdf/doi/10.1257/jep.15.4.101), they use a 66% confidence level. While they did not explain why 66, not 95, I guess it makes some IRFs (which would be insignificant at 95%) more significant. For example, in their original paper, interest rate shock to inflation appears significant at a 66% confidence level, but my estimation at a 95% confidence level shows it is not significantly different from zero. I am not criticizing this paper or anything like that, but it appears the choice of the level of confidence is at the discretion of the researcher, either arbitrarily or purposefully. If this is not the case, what would make one choose a confidence level of 66% and not 95%, or even 99%?