Textbooks still include discussion of money multiplier together with more nuanced discussion of central banks setting interest rates (compatible with story in McLeay et al 2014). In fact they did so already before the paper was published in 2014.

I think in order to answer this question it will be important to first correct a misconception you seem to have about what the paper implies regarding to textbook story. You state:

The paper is damming about the description of the monetary system as given in many undergraduate level textbooks.

No. If you actually read McLeay et al 2014 they state:

While the money multiplier theory can be a useful way of

introducing money and banking in economic textbooks, it is

not an accurate description of how money is created in reality.

Rather than controlling the quantity of reserves, central banks

today typically implement monetary policy by setting the

price of reserves — that is, interest rates.

Consequently, the paper was certainly not damming of the textbook money multiplier story (and no fair reading of the paper can conclude they went as far as damming the description of whole monetary system in textbooks which goes way beyond just money creation), and going by this statement I doubt that the authors would even want to remove this story from textbooks as they themselves consider it useful. I also can't see anything else in the paper that would suggest that multiplier should not be included in the textbooks as a didactic tool (e.g. analogously most markets are not perfectly competitive, yet I don't think that economic textbooks will ever be able to efficiently introduce more complex market structures before discussing case of perfect competition no matter how unrealistic such market structure might be).

Now onto your main question, one of the main point of McLeay et al (2014) is that:

Rather than controlling the quantity of reserves, central banks

today typically implement monetary policy by setting the

price of reserves — that is, interest rates.

Now this is something that was already discussed in textbooks quite long time ago. Let me give you some examples:

Blanchard et al. Macroeconomics an European Perspective. 2nd ed. Widely used mainstream textbook with 2nd edition published in 2013 (year before the paper came out), states pp 69-70 (square brackets contain my remarks):

We have described the central bank as choosing the money supply and letting the interest rate be determined at the point where money supply equals money demand [i.e. the multiplier story]. Instead, we could have described the central bank as choosing the interest rate ... Why is it useful to think about the central bank as choosing the interest rate? Because this is what central banks, including the ECB, the Bank of England and the Fed, typically do...

the textbook then proceeds to give simplified down narration of what you could have read in the 2014 paper (but remember this is undergraduate textbook everything is simplified there).

Mankiw Macroeconomics 8th edition - originally published in 2012, states:

Although it is often convenient to make the simplifying assumption that the

Federal Reserve controls the money supply directly, in fact the Fed controls the

money supply indirectly using a variety of instruments. ...

There are various ways in which banks can borrow from the Fed. Traditionally,

banks have borrowed at the Fed’s so-called discount window; the discount rate

is the interest rate that the Fed charges on these loans. The lower the discount

rate, the cheaper are borrowed reserves, and the more banks borrow at the Fed’s

discount window. Hence, a reduction in the discount rate raises the monetary

base and the money supply.

In recent years, the Federal Reserve has set up new mechanisms for banks

to borrow from it. For example, under the Term Auction Facility, the Fed sets a

quantity of funds it wants to lend to banks, and eligible banks then bid to borrow

those funds. The loans go to the highest eligible bidders—that is, to the banks

that have acceptable collateral and are offering to pay the highest interest rate.

Unlike at the discount window, where the Fed sets the price of a loan and the

banks determine the quantity of borrowing, at the Term Auction Facility the Fed

sets the quantity of borrowing and a competitive bidding process among banks

determines the price. The more funds the Fed makes available through this and

similar facilities, the greater the monetary base and the money supply.

In fact the last paragraph was addition to the 8th edition that was not there in 7th edition (published in 2010) so you can see these textbooks usually catch pretty quickly.

Burda & Wyplosz Macroeconomics: A European Text 217-218 3rd ed, originally published in 2009:

Nowadays, ... most central banks choose to control the interest rate ... a central bank can set any interest rate it chooses, provided it stands ready to provide or withdraw liquidity in any amount needed to meet the derived demand corresponding to this rate.

the textbook then proceeds to discuss basically what is the point of the 2014 paper already in 2009.

The newer editions of the books that were printed post 2014 still contain this explanation. But given that they already addressed this issue prior 2014 I would not attribute it to McLeay et al paper per se. As clearly shown above textbooks addressed this issue already in 2009.

You can see these chapters being further expanded in the newer editions of the Mankiw and Blanchard et al Macro textbooks. Perhaps this further expansion can be attributed to influence of McLeay et al paper. Arguably Blanchard et al do this at much greater length then in Mankiw textbook.

In addition, it is worth to point out that I do not think that the above shows that McLeay et al were being duplicitous in their 2014 paper. In fact, if you read the paper carefully they never state that textbooks do not cover how money is being created by modern central bank. They always refer to money multiplier story (that admittedly is given perhaps too much space) in the textbooks that they are trying to 'debunk' but they actually never state that textbooks do not cover that modern central banks conduct monetary policy through interest rates.

Response to Edits:

I would suggest that there are two distinct issues that McLeay et al are complaining about:

A) Incorrectly suggesting that banks lend deposits rather than correctly stating that lending creates deposits.

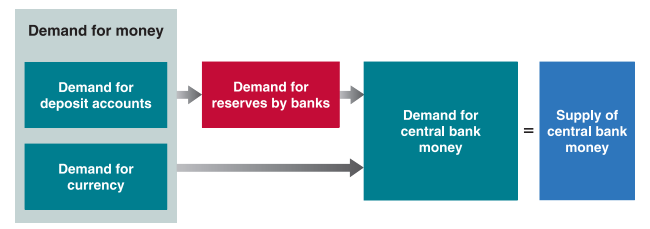

I cant find a passage where McLeay et al state that textbooks got this point wrong, but if they state that somewhere it would be incorrect. In fact, this is a picture that is from the above cited Blanchard et al Macro textbook pp 71 from 2013!

The picture clearly shows that demand for deposits creates demand for reserves which is exactly the point of McLeay paper. In addition there is nothing wrong in principle also arguing that from supply side the increase in supply of reserves would lead to increase in borrowing and deposit accounts. It is not the mode of behavior that modern central banks would choose but it is not wrong in itself as they could do that. The relationship in the diagram above has to hold but of course central bank has discretion in deciding whether to change interest rate (which affects the demand for money and then you get the effects coming from deposits) or to change supply of money directly where the effect would go opposite way. It is correct to state that modern central banks usually choose former rather than latter (and as proven above textbooks acknowledge that), but that does not mean it’s wrong to say that central banks could conduct monetary policy via direct changes in money supply.

B) Incorrectly suggesting that the money supply has a ceiling set by reserve requirements in practice.

Regarding, the B they nowhere say that reserve requirements do not create celling for lending. They state instead that banks will lend out money and then seek to raise their reserves by purchasing them on interbank market in order to maintain the mandatory reserve ratio - but they have to maintain that ratio.

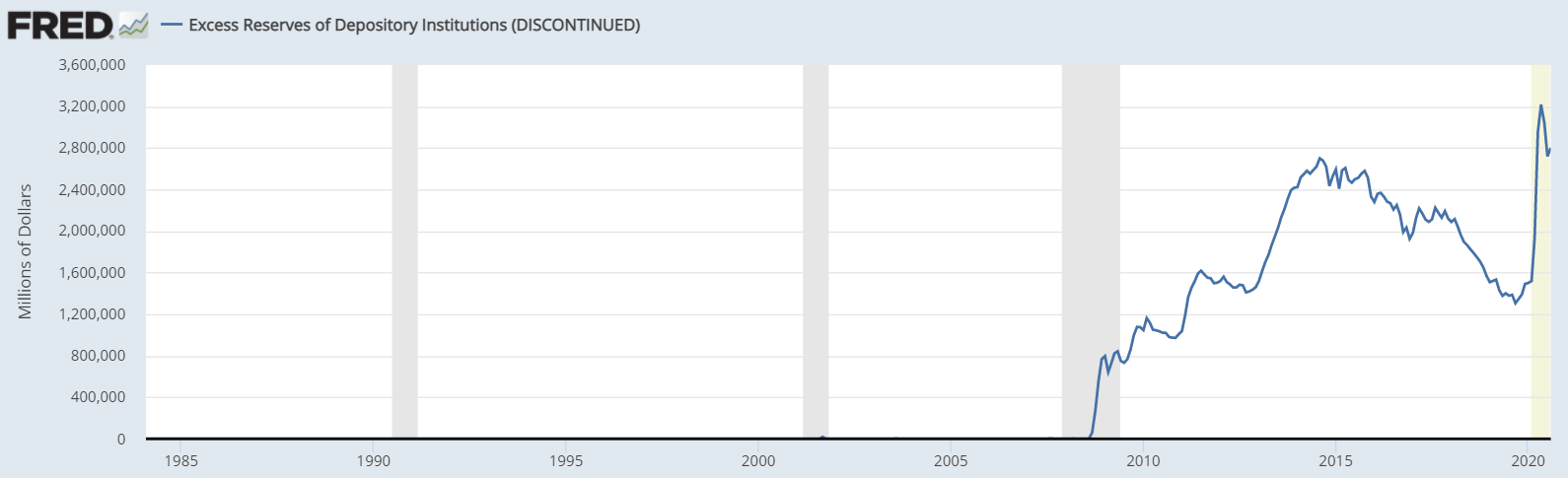

First of all, as you can see from the statistics on excess reserves below (which is discontinued now as reserve requirements were abolished in 2020), prior 2009 banks held virtually no excess reserves. In such situation the amount of reserves supplied by central bank is hard cap for lending of commercial banks. If they would lend more they would literally break the law (as a tidbit in such situation the multiplier story still applies as the ratio to reserves and broad money should be approximately given by the multiplier). After 2009 market held excess reserves, in that situation you can think of every individual bank be unconstrained by reserve requirement because without central bank doing anything any individual bank can borrow excess reserves from any other bank to maintain their reserve requirement (this is what they mean in the paper when they say banks are unconstrained by reserves). However, the banking system as a whole (all banks taken together) is still constrained by the reserve requirement and amounts of reserves. Even in this situation banks could not all at the same time lend more than they can given the reserves and reserve requirement. So this is not something that textbooks, which are written from the perspective of whole system rather than single bank, get wrong (and again I cant see them calming that textbooks do that in the paper). In fact here you could actually coitize the McLeay et al for not being careful enough about explaining this.