For example, in a three-variable SVAR model in Favero, C. A. (2001), the author uses Cholesky decomposition to identify only money shocks by ordering it last. Thus, both $p_t$ and $y_t$ affect $m_t$ contemporaneously, and this is the only identification condition in the model.

He mentions that the identification of shocks to $p_t$ and $y_t$ do not matter in the model. We can see here that $p_t$ affects $y_t$ contemporaneously but not the reverse.

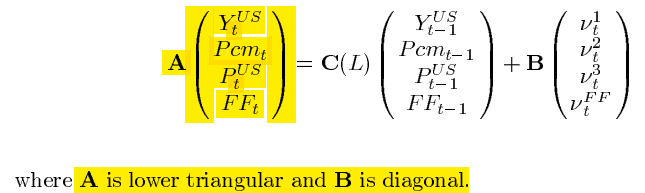

In another example in the same book, $y_t$ contemporaneously affects $p_t$ which is in contrast to the example above. Again, he seeks to identify shocks only to $FF_t$, and hence does not discuss the ordering of the non-policy block of the model. I guess it is arbitrary.

I see same thing in Primiceri, G. E. (2005). Interest rates are ordered last in the VAR. The interaction between inflation and unemployment is arbitrarily modeled in a lower triangular form, with inflation first, unemployment second. So I guess unemployment could also be first.

Another example is by Drechsel, T., & Tenreyro, S. (2018). There are 4 variables in the VAR. The only identification condition is that commodity price is ordered first in the lower triangular Cholesky identification scheme. The author does not mention how the other 3 domestic variables are arranged in the model. So I guess, arbitrarily.

So my question is, in a lower triangular Cholesky identification scheme, one does not necessarily need to have an economic theory for all the orderings of the variables in the model, right? I mean, some of the orderings can be arbitrary if one do not care about the shocks associated with these aribitrarily ordered variables in the model?