Printing Greenbacks During the Civil War

Lincoln’s Greenback Mill: Civil War Financing and the Start

of the Bureau of Engraving and Printing, 1861–1863

http://shfg.org/resources/Documents/FH%201%20(2009)%20Noll.pdf

Faced with a breakdown of its

war financing scheme because of the failure of bank note companies to produce the needed currency and bonds, the Treasury Department was forced on an ad hoc basis to enter the printing

business to meet its needs.

Historically during the Free Banking era gold and silver were specified as money. In theory any private or public institution could mint gold and silver coins. Also in theory anyone could issue currency notes provided others would accept the notes instead of payment in silver and/or gold. Banks would order their own brand of currency notes from private bank note printing companies. During the Civil War the government finance concerns drastically altered both the government customs and financial customs because the Treasury became an even more dominant institution in the financial system.

How Currency Gets Into Circulation

https://www.newyorkfed.org/aboutthefed/fedpoint/fed01.html

The public typically obtains its cash from banks by withdrawing cash from automated teller machines (ATMs) or by cashing checks.

To meet the demands of their customers, banks get cash from Federal Reserve Banks. Most medium- and large-sized banks maintain reserve accounts at one of the 12 regional Federal Reserve Banks, and they pay for the cash they get from the Fed by having those accounts debited. Some smaller banks maintain their required reserves at larger, "correspondent," banks. The smaller banks get cash through the correspondent banks, which charge a fee for the service. The larger banks get currency from the Fed and pass it on to the smaller banks.

When the public's demand for cash declines—after the holiday season, for example—banks find they have more cash than they need and they deposit the excess at the Fed. Because banks pay the Fed for cash by having their reserve accounts debited, the level of reserves in the nation's banking system drops when the public's demand for cash rises; similarly, the level rises again when the public's demand for cash subsides and banks ship cash back to the Fed. The Fed offsets variations in the public's demand for cash that could introduce volatility into credit markets by implementing open market operations.

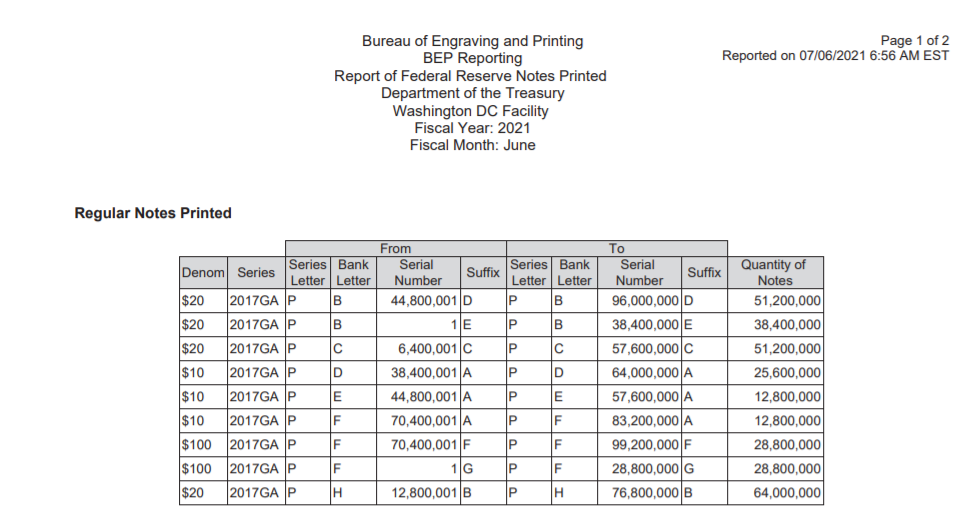

The Federal Reserve orders new currency from the Bureau of Engraving and Printing, which produces the appropriate denominations and ships them directly to the Reserve Banks. Each note costs about four cents to produce, though the cost varies slightly by denomination.

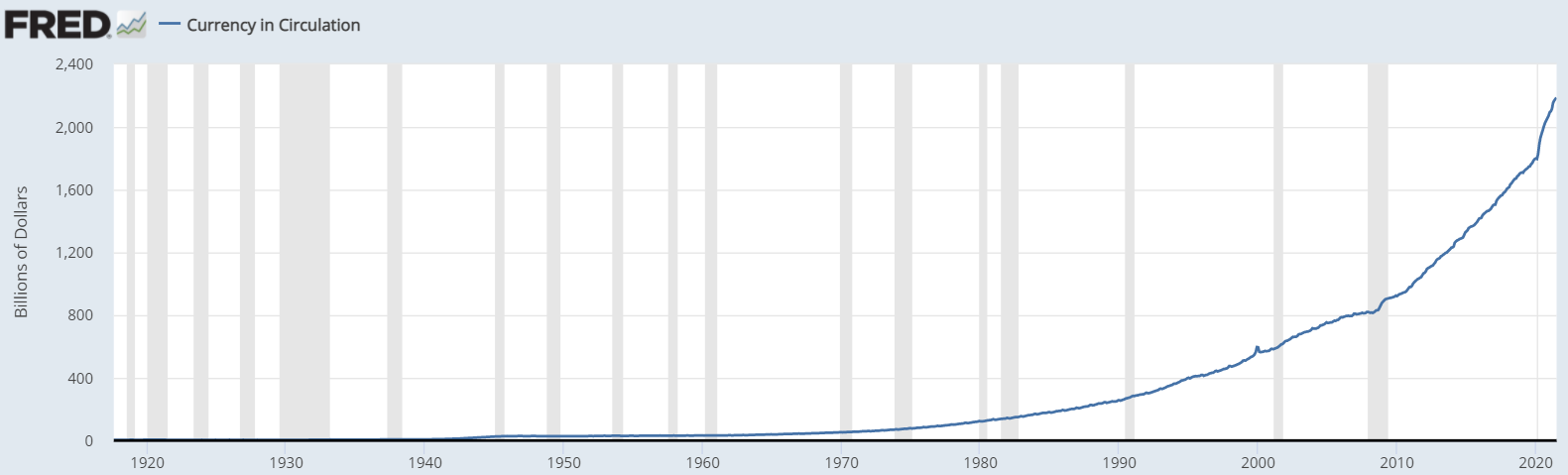

Virtually all of currency notes in use are Federal Reserve notes. Each Federal Reserve Bank is required by law to pledge collateral at least equal to the amount of currency it has issued into circulation. The bulk of the collateral pledged is in the form of U.S. Government securities and gold certificates owned by the Federal Reserve Banks.

Comments

Financial assets:

- Vault cash

- Reserve balances

- Currency outside banks

- Transaction deposits

- Treasury securities

The M1 money supply consists mostly of transaction accounts in the aggregate bank and Federal Reserve Notes in circulation.

Banks use vault cash to service withdrawal of currency by their customers. Banks use reserve balances at Fed to clear interbank payments and payments with Fed and/or other government agencies kept in the books of the Treasury Department. The government and non-banks clear payment using reserve balances and transaction deposits which is a two-tier payment clearing system.

The M1 money supply does not increase by the government printing money to deficit spend because the federal government issues net new Treasury securities to cover the deficit. Treasuries are considered to be risk-free financial assets which exchange easily for money so the money markets are made more liquid via the increase of Treasuries when the government pays for the deficit via the issue of Treasuries.

The state and federal governments enable the bank sector, via the banking franchise, to provide the elastic money supply by making credit entries to bank deposit accounts. A liability account increases by a credit entry; deposits are liabilities of the bank and bank sector; when net new credit entries are made on the books of the aggregate bank sector the money supply increases via the customs of double-entry accounting and via the legal recognition of finance relations. If these credit entries are made in paper ledgers or books, then money supply increases via recording such symbols in books. If these credit entries are made in electronic storage media then the money supply increases electronically. However the money is printed and/or otherwise issued via the debtor-creditor laws and accounting customs. The means of printing notes or keeping records of money as an accounting symbol rather than as a tangible symbol in token form (notes, coins) is just part of the financial game.

So banks increase the money supply when they issue net new loans to non-bank customers or purchase securities from non-bank sellers. If bank customers withdraw funds over time then this would drain reserve balances of the bank sector held at the Fed because banks pay the Fed for currency using reserve balances. If Fed purchases securities from non-banks in the open market, however, to hold as assets equal to the amount of currency in circulation, then Fed would be putting reserve balances and deposits back into the aggregate bank sector, meaning the withdrawal of currency would increase the currency portion of M1 money without reducing the deposit portion of M1 money other factors being equal. However other factors are not equal because non-banks can convert deposits in M1 to saving or time deposits in M2 money supply or into other bank liabilities or equity via portfolio allocation decisions.

Therefore banks increase the money supply via the increase of bank assets, if Fed offsets the currency drain then banks do not have to decrease the aggregate bank balance sheet to service this drain, and the mix of currency and deposits in M1 money supply is a non-bank portfolio allocation decision enabled by the system where Fed purchases money from the Mint for distribution to the banks for distribution to bank customers.