Question

How should I deal with missing data when trying to test the CAPM? Specifically, there are some stocks that are newly listed and/or delisted at any time. I don't want to exclude assets for which I don't have complete data because this would create a kind of survivor bias. I know that CRSP provides delisting returns that should, but how do I manage the missing data in practice? For example, in the unconstrained model, the procedure looks like this:

(More details about the procedure are given below.) Now, if I wanted to take a bunch of random stocks at some point in time and look at them over some time period, what should I do with the values ($Z_it$) for these stocks that aren't listed at time $t$. Should I use the de-listing returns where appropriate and then fill in zeros everywhere else? But this would do weird things to the beta of the stock. Should I try to constrain the beta (the factor loadings) of the stocks to be zero in all the places where the stock is unlisted? This would require me to change the model (requiring a model that somehow allows for time varying factor loadings). How do people usually handle this problem? Is there an easy way (even if it is slightly more incorrect)?

Some Detail about the Estimation Procedure

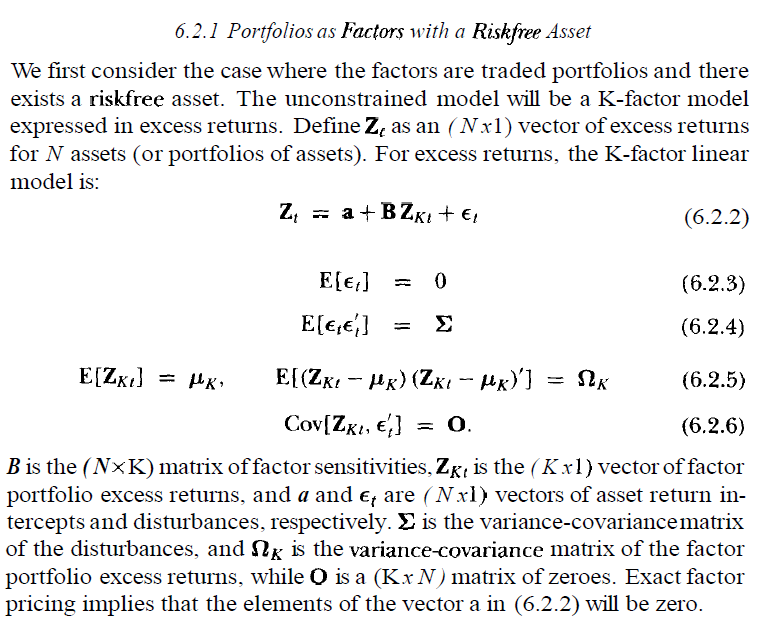

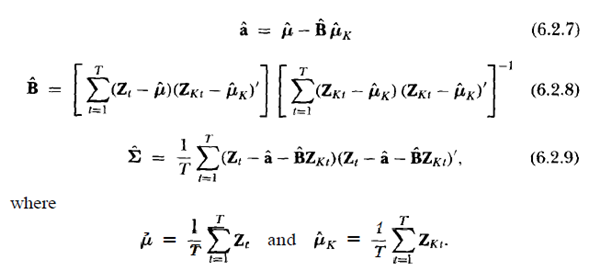

For concreteness, suppose I wanted to test the CAPM using the time series regression framework outlined in chapter 6 of Campbell, Lo, and MacKinley (The Econometrics of Financial Markets). Some of the assumptions are listed in this image: