Output elasticity of an input means (consider the non-calculus formulation) the percent change in output for a percent change in input (it is customary to substitute “change” with “increase”).

Let’s say, we have a production model: $$ P= A x_1^{a_1} x_2^{a_2} \cdots x_n^{a_n}$$

Where, P is the estimated production, $x_i$ are inputs and $a_i$ are corresponding output elasticities.

If from a data for last ten years we perform a Multilinear Regression Analysis and found that some $a_i$ is negative, what does it mean in physical sense? Because, $x_i$ is needed for production, but why its increase by a percent decreases the production? Doesn’t that imply: it is not wise to employ $x_i$ at all?

In sense the production is inversely proportional that input, as $$ P \propto \frac{1}{x_i^{a_i}}$$

But then why to take something in production whose increase diminishes the production?

ADD-ON:

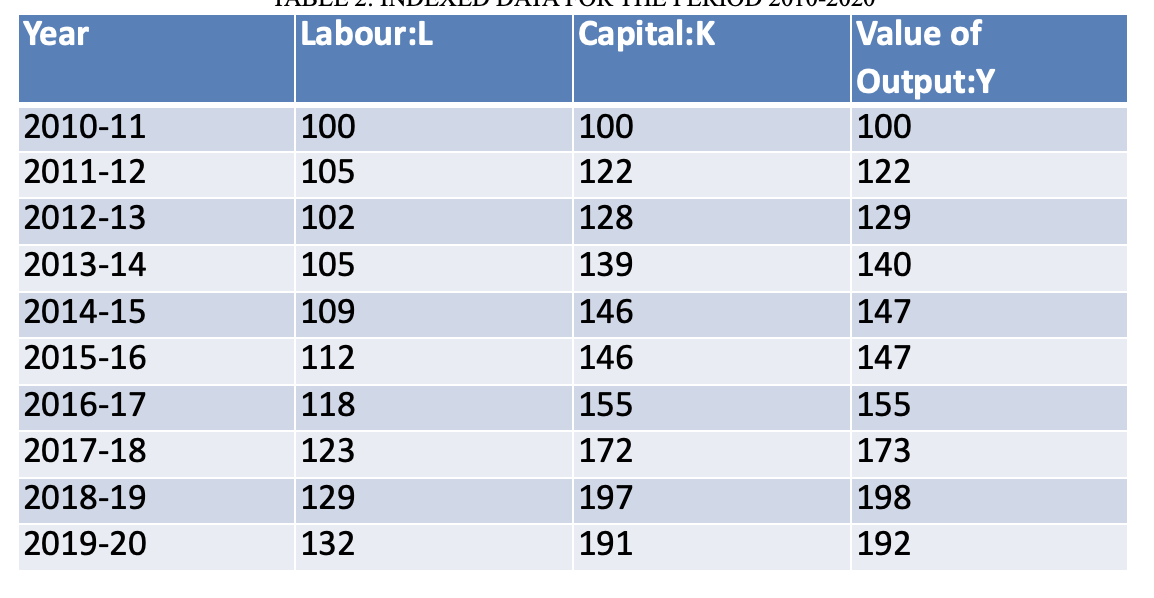

I performed Multi linear Regression Analysis (zero intercept is not forced) using the Software StarPlus, available on Mac's App Store, on the Cobb-Douuglas Function: $$ P = A L^{\alpha} K^{\beta}. \\ \ln P = \ln A + \alpha\ln L + \beta \ln K$$

using the data of Indian Manufacturing Sector:

the values of data are indexed with base period 2010-11.