I often see that the theory of sticky wages is cited as an explanation for an upward sloping short run aggregate supply curve. I understand that if aggregate demand shifts to the left, there will be downward pressure on price level. A lower price level means that in the labor market, if the nominal wage stays sticky, the real wage will increase. This disincentivizes hiring and will cause employment below the natural level, which causes real GDP to fall below the potential.

However, I do not understand how a rightward shift in aggregate demand results in an increase in real GDP.

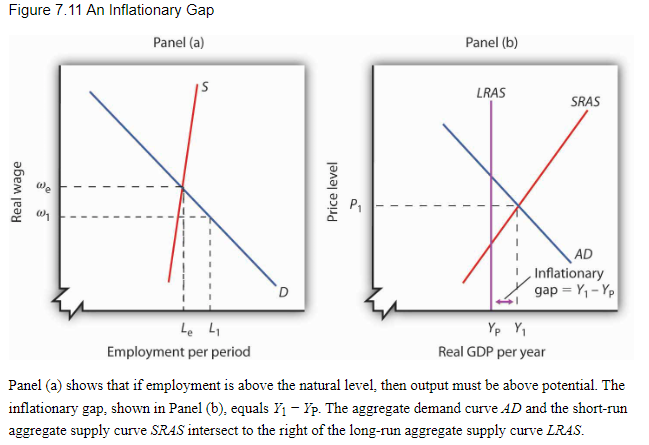

By the same logic as before, a rightward shift in aggregate demand will cause upward pressure on price level, and (with sticky wages) will lower the real wage. My textbook says that, in the labor market, this will move along the demand curve for labor:

However, this seems to contradict what I thought was the definition of the factor market supply curve. I would have expected that too low of a real wage would also result in less than natural employment due to a shortage of workers.

How is it possible that people will ever give more labor than they are willing to supply at a given price?

Where is my reasoning wrong?