Explicit Reasoning

This post is edited substantially in the hope of clarifying how credit flows increase, decrease, or do not increase or decrease the levels taken to be the statistical measures of the elastic money supply in the depository institutions.

Simplified Bank Balance Sheet and Income Statement

Loan Loss Reserve Accounting and Bank Behavior (4 pages)

Bank assets are classified broadly as either Bank Credit or Total Reserves. In the paper above "Cash" would correspond to and contribute to "Total Reserves" of the Depository Institution sector. Bank Credit would include Loans and all other financial assets held by each bank but would specifically exclude reserves. The bank sector uses reserve balances at the central bank to clear interbank payments and uses vault cash to service withdrawals of currency from the bank.

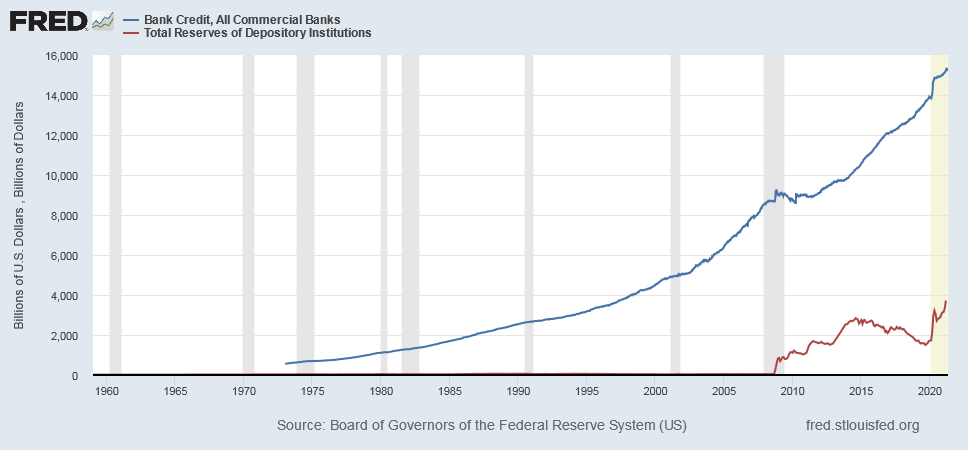

This graph shows that US Bank Credit grows historically without a corresponding increase in Total Reserves prior to the US financial crisis of 2007-2008:

One may infer that the Bank sector, also known as Depository Institutions sector, does not require a net increase in total reserves to expand Bank Credit at least over the period shown prior to the 2007-2008 crisis. Then the question is how the depository institutions expand bank credit without a significant increase in total reserves?

When a bank expands Bank Credit it would initially debit a financial asset account for an increase and usually it would credit a checkable deposit account for an increase. The checkable deposit category is a major component of the M1 money supply. So the expansion of bank credit increases the money supply in most cases initially as M1. However in the complex banking sector a bank can induce its customers to move funds from M1 to time/saving deposits which are in M2 money supply. So the basic idea is that a bank or bank sector increases the money supply by the expansion of financial assets other than its vault cash or reserve balances.

If the checkable deposit is spent to another customer of the same bank then the bank will credit the deposit account of the payee for an increase and debit the account of the payor for a decrease with no change in total deposits. So the money supply does not increase or decrease for this type of transaction and the bank does not have to pay reserve balances to transfer funds among its own customers.

If the checkable deposit or other deposit funds transfer to the customer of a second bank then the first bank must credit reserves balances (Cash in the paper above) for a decrease and debit deposits for a decrease. The second bank would debit reserve balances for an increase and credit deposit funds for an increase. These transactions do not change levels of reserves or deposits they simply move reserves and deposits from a first bank to a second bank by the payment instructions and double-entry accounting customs applies at each bank. Note each bank is like a "node" in a communication network which receives payment messages and executes the accounting operations necessary to change its records. This is how the payment mechanism works whether kept in books of account or electronic records stored in digital media.

The first bank (like any bank) will be depleted of reserve balances if it expands bank credit but fails to expand interest paying deposit liabilities and/or paid-in equity claims which force a flow of reserves back into the bank to clear the interbank payment on its expansion of the balance sheet.

Suppose a bank cannot expand interest paying deposits and/or paid-in equity then how does it make interbank reserve payments? It either borrows reserve balances from another bank in the overnight market for federal funds; or it borrows from the central bank at the "penalty" rate also called the "discount window" rate which is usually set above the monetary policy target rate; or it sells securities out of its asset portfolio. The sum of total reserves and securities is the liquidity cushion which each bank holds to make interbank payments when it has difficulty expanding the liabilities and paid-in equity side of the balance sheet.

The Financial Accounts Guide All Tables

https://www.federalreserve.gov/apps/fof/FOFTables.aspx

Scrolling down one observes financial statistics tables organized as Sectors: Transactions (links in the left side column) and Sectors: Levels (links in the right side column).

Transactions in these financial tables are classified as economic flows. These are financial flows caused by credit/debt deals.

Levels in these financial tables are economic stocks. The creditors own financial assets and the debtors owe liabilities or debts to the creditors. The flows of credit/debt deals increase or decrease the stocks of financial assets and liabilities because the financial tables are designed to be stock-flow consistent in accord with legal interpretations of credit/debt instruments and accounting customs for recording financial assets with matching liabilities.

Levels of Monetary Authority (Fed)

https://www.federalreserve.gov/apps/FOF/Guide/L109.pdf

Note three liabilities of the Fed are counted in the base money supply or monetary base also known as MB or M0:

Depository institution reserves

Vault cash of depository institutions

Currency outside banks

FRB H.4.1 Release shows Factors Supplying Reserve Balances including Reserve Bank credit and other assets listed on the Fed balance sheet:

https://www.federalreserve.gov/releases/h41/current/

FRB H.4.1 Release also shows Total factors, other than reserve balances, absorbing reserve funds including currency in circulation and all Fed liabilities other than reserve balances.

So Fed manages the level of reserve balances by using Reserve Bank credit to supply reserve balances when necessary if other factors absorb reserve balances. Some items on the balance sheet are autonomous, or not under the control of Fed, and other items are control factors such as levels of Reserve Bank credit. The flow of Reserve Bank credit is used as a control factor to supply levels of reserve balances against factors absorbing reserve balances as necessary to support the monetary policy goals of the Monetary Authority.

Levels of Private Depository Institutions

https://www.federalreserve.gov/apps/FOF/Guide/L110.pdf

Currently the first three lines are Total financial assets, Vault cash, and Reserves at Federal Reserve. Assume non-financial assets are negligible compared to the magnitude of financial assets. Then define Bank Credit:

Bank Credit = Total financial assets - Vault cash - Reserve balances

Depository institution liabilities are simplified by definition of Bank sector Liabilities* which are not classified as Checkable deposits:

Liabilities* = Total liabilities - Checkable deposits

The difference between bank assets and liabilities in the levels tables can be designated as equity claims or net worth to visualize a complete balance sheet:

Equity = Total Assets - Total Liabilities

Reasoning by analogy to the Monetary Authority balance sheet, which gives the factors supplying reserve balances and the factors absorbing reserve balances, the Depository institutions balance sheet would have factors supplying Checkable deposits and factors absorbing checkable deposits. We can write these factors in an identity as follows:

Checkable deposits = Reserve Balances + Vault Cash + Bank Credit - Liabilities* - Equity

where a transaction in the aggregate bank sector can increase or decrease Checkable deposit levels due to double-entry accounting customs. The sum of Checkable deposits and Currency outside banks is called the M1 money supply. The sum of Checkable deposits and items in Liabilities* is the M2, M3, etc. money supply. Liabilities* include items that are not counted in aggregate measures of the money supply so money supply is created, destroyed, or conserved depending on the nature of the transaction as a flow that supplies or absorbs or does not alter whatever definition of the "money supply" is applied for analysis.

Bank Credit Expansion or Contraction

${\Delta}$ Checkable deposits = ${\Delta}$ Bank Credit; or

${\Delta}$ Liabilities* = ${\Delta}$ Bank Credit; or

${\Delta}$ Equity = ${\Delta}$ Bank Credit;

In most cases the depository institution or bank sector originates credit by putting funds into the checkable deposit accounts of bank borrowers or bank customers who have sold financial assets to the bank. When bank sector sells a financial asset to units outside the sector, or when a bank customer outside the bank sector repays a loan the bank sector, the bank sector would reduce its sum of liabilities and equity and reduce assets listed in bank credit.

Changing the Mix of Depository Institution Liabilities and Equity

${\Delta}$ Checkable deposits + ${\Delta}$ Liabilities* + ${\Delta}$ Equity = 0

When banks induce customers to change the mix of liabilities and equity by offering interest on liabilities and dividends or hope for capital gains on equity this is a zero sum game which does not increase or decrease the bank balance sheet.

If a bank fails to expand Liabilities* and Equity as it expands Bank Credit then it would be depleted of reserve balances via the payments it does make and then it would unable to make interbank payments except to sell assets out of its Bank Credit portfolio. So a bank or aggregate bank sector grows via the increase of Bank Credit, Liabilities* (which are not Checkable deposits), and Equity.