I am aware that Monte-Carlo Simulation is used for making accurate assumptions by introducing randomness. But can it be used to synthesize or create a dataset? If yes, can someone share an example?

$\begingroup$

$\endgroup$

0

Add a comment

|

2 Answers

$\begingroup$

$\endgroup$

YES

I’ll give an example in R.

set.seed(2022)

# Set sample size

#

N <- 100

# Declare some regression feature

#

x <- seq(1, 100, 1)

# Define the outcome variable, using a

# random normal error term (this is

# the Monte Carlo part)

#

y <- 1 - x + rnorm(N)

Now your have a synthetic data set and can run a regression, for instance.

An example of where this might be useful is if you develop a new hypothesis test for a regression coefficient and want to see how it performs when the null hypothesis is true. Thus, you loop through $1000$ regression simulations like this and hypothesis test each time, collecting the p-value of each hypothesis test.

set.seed(2022)

N <- 100

R <- 1000

ps <- rep(NA, R)

x <- seq(1, N, 1)

for (i in 1:R){

y <- 1 + rnorm(N) # zero slope coefficient

L <- lm(y ~ x)

ps[i] <- summary(L)$coef[2, 4] # extract p-value of t-testing slope

}

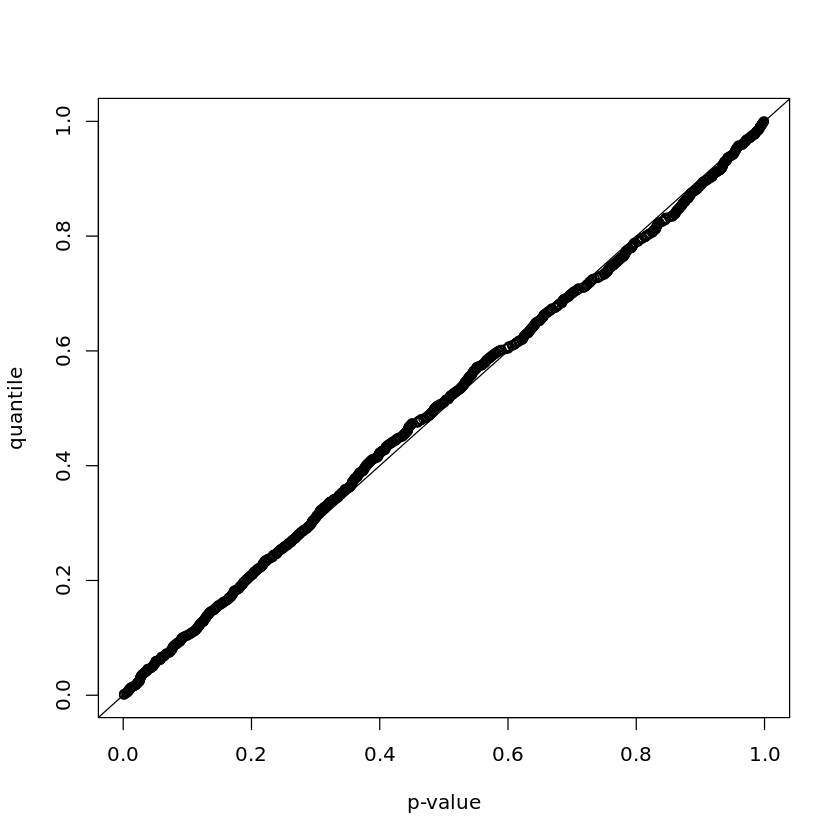

plot(

ps,

ecdf(ps)(ps),

xlab = "p-value",

ylab = "quantile"

)

abline(0, 1)

If you were the inventor of the t-test used here, you would see that your test gives uniform p-values under the null hypothesis of zero slope (exactly the desired behavior).

$\begingroup$

$\endgroup$

The library TensorFlow Probability is designed for this purpose. In fact, the first example currently at the web site involves the creation of synthetic data which is then used for a regression example:

import tensorflow as tf

import tensorflow_probability as tfp

# Pretend to load synthetic data set.

features = tfp.distributions.Normal(loc=0., scale=1.).sample(int(100e3))

labels = tfp.distributions.Bernoulli(logits=1.618 * features).sample()

# Specify model.

model = tfp.glm.Bernoulli()

# Fit model given data.

coeffs, linear_response, is_converged, num_iter = tfp.glm.fit(

model_matrix=features[:, tf.newaxis],

response=tf.cast(labels, dtype=tf.float32),

model=model)

# ==> coeffs is approximately [1.618] (We're golden!)