I'm a new economics student, and have become fascinated by the field of Industrial Organization. To that end, I'm reading through the Carlton and Perloff Modern Industrial Organization text book. In doing so, I have come upon a question I was hoping to ask the group here. If all product markets are perfectly competitive (to a reasonable approximation), shouldn't the returns to invested capital (a way of measuring 'economic profit') in every product market, whether the market be for cement or GPS integrated circuits, be equivalent after adjusting for risk? Or put in a equivalent way, do the differences that are seen (in reality) between the rates of return in different businesses/industries reflect purely differences in risk borne by shareholders/capital-owners?

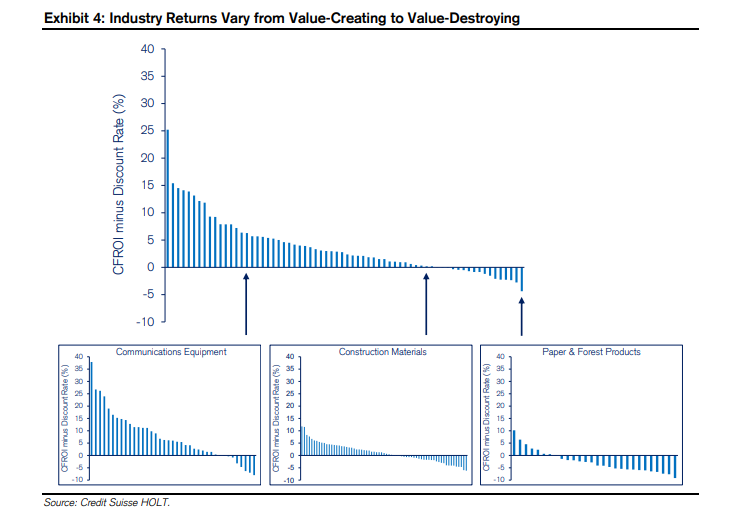

The reason I ask is because it seems (to my untrained eye) as if the assumption that all markets have equal risk-adjusted rates of return is just manifestly not true (see the graph below). Different product-markets and indeed different firms within a particular market empirically show wide variance in profits and returns (can provide some sources if needed). If the difference is not driven merely by risk, what explains this difference and what are the welfare implications of that explanation?

This leads me to the true question I'm interested in answering. If high returns in certain markets are not explainable by risk, then are they entirely ascribable to market power (with its attendant losses to overall welfare and efficiency)? Or could there be other factors at play? If there are other factors at play, what are they and can you point or direct me to models/theories/papers which describe them? One factor that some people throw around colloquially is "efficiency"; a firm might be more efficient than its competitors. What models explicitly model the process of a more efficient firm and its attend effects on returns, profits and welfare?

Of course, I might be missing something huge. I am new to this and am asking what I realize to be very naive questions. Happy to be educated :)

Edit: I realized that there might have been some confusion. I was referring to differences in rates of return between and within different product markets, not different countries. So the phenomenon I'm interested in understanding is the following graph, which is taken from here