Guvenen et al look at earnings shocks over time, and try to argue whether these are compatible with standard career-ladder models with normal shocks.

However, their data is no real shocks, it is time differences in labor earnings. We do not know which part of these were expected. What are things to consider if one tries to take into account for the fact that these income changes are - to some extent - expected ex ante?

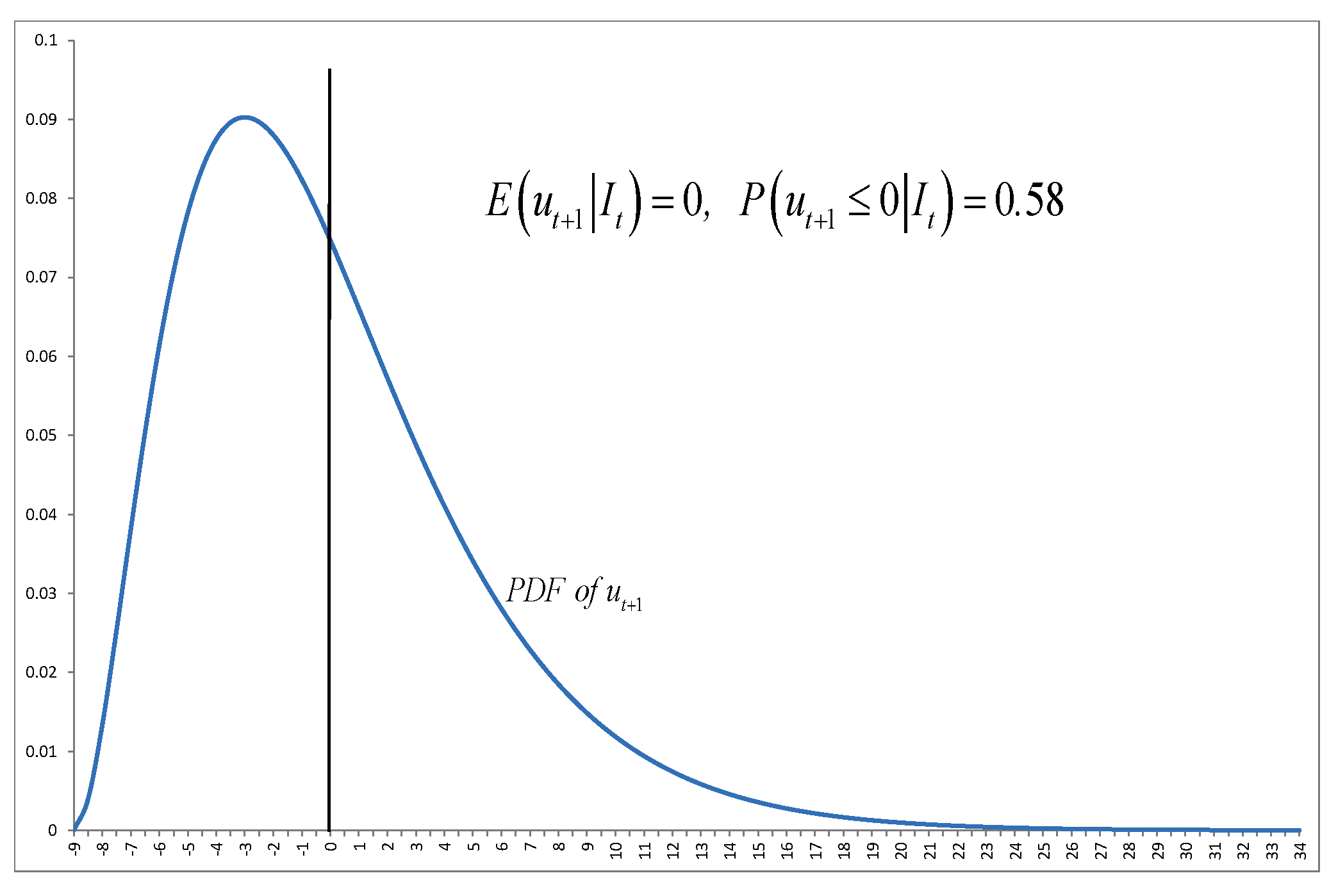

My first guess would be that since people expect future rise in income, correcting the "shocks" for that would mean that the unexpected part of the shocks is to the left of their yearly changes in wage income. That is, there are more shocks downwards than upwards.