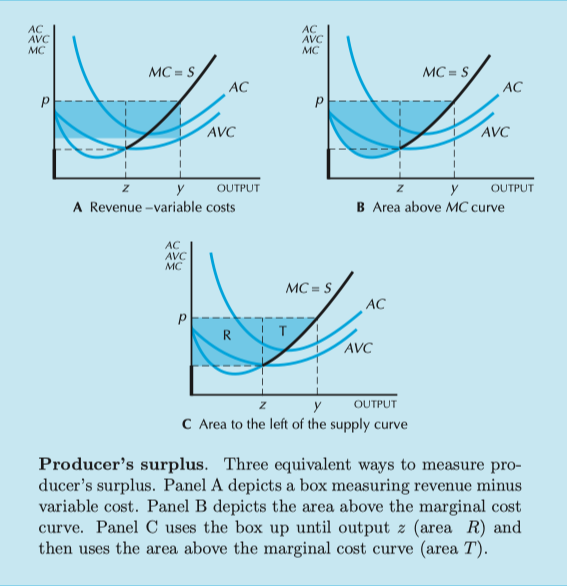

In the Firm supply chapter of the microeconomics Varian's book, they show "three equivalent ways to measure producer’s surplus" using marginal cost, average cost and the average variable cost curves.

But my teacher says, "those three ways give different results. You have to keep the same method during a given analysis".

So are they or not giving the same result?

Intuitively I think they do give the same result and do not understand why my teacher says they do not.