Well i just edited my answer a lot. I made a fundamentally mistake, from $ L_ {h} $ arises an unique value of h, even when $ h $ is in other first order conditions, that doesn't change anything. Once that i have clear that there is no relationship between $ \beta $ and $ h $, I think I know what is happening.

The reason why it is invested in $ h $ although $ \beta = 0 $ is because h increases the NPV, and this allows to increase consumption in the first period. What happens is $\beta=0 \ \Rightarrow \ \ c_{2}=0$. But let´s see this more carefully.

To do this we have to add restrictions to the model $c_{1},c_{2},h > 0$, so the lagrangian will change:

\begin{align}

L= L = u(c_1) + \beta u(c_2) + \lambda_{1} \left( y - h + \frac{w(h)}{1+r} - c_1 - \frac{c_2}{1+r} \right) +\lambda_{2}c_{1}+\lambda_{3}c_{2}+\lambda_{4}h

\end{align}

The new first order conditions will be:

\begin{align}

\frac{\partial L}{\partial c_{1}} = u^{ ' }(c_{1}) - \lambda_{1} + \lambda_{2} =0 \ (1)\\

\frac{\partial L}{\partial c_{2}} = \beta u^{ '}(c_{2}) - \frac{\lambda_{1}}{1+r} + \lambda_{3}=0 \ (2)\\

\frac{\partial L}{\partial h} =(\frac{ w^{ ' }(h)}{1+r} -1)\lambda_{1} + \lambda_{4}= 0 \ (3)\\

\end{align}

But we need for constraints with inequalities the complementary slackness conditions (we can work with the Kuhn-Tucker lagrangian, but that it's just a special case of this general formulation):

\begin{align}

\lambda_{1}(y-h + \frac{ w(h)}{1+r} - \frac{ c_{2}}{1+r}-c_{1}) =0 \ (4) \\

\lambda_{2}(c_{1})=0 \ (5) \\

\lambda_{3}(c_{2})=0 \ (6) \\

\lambda_{4}(h)=0 \ (7) \\

\end{align}

This means that either the restriction or the $\lambda_{i}$ will be 0. To solve this equations we need to exhaust all posibilities, and see if we can arrive to a solution that is consistent or discard cases that lead to contradiction. Im going to show that $\beta=0 \ \Rightarrow \ c_{2}=0, \ h=constant$. You can look for yourself to check if there is other posible solutions.

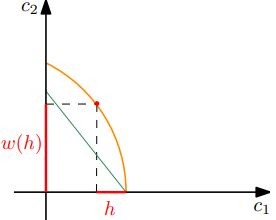

So let's see if $\beta=0 \ \Rightarrow \ c_{2}=0, \ h=constant$ it's a solution. if $\beta=0$ the logical thing would be to think that the optimal solution would be $c_{2}^{*}=0$, so let's just assume that this it's the case, if it is not, at some point the first order conditions must show that this is not consistent.

Also, we expect that $c_{1}>0$ which implies by (5) $\lambda_{2}=0$. We can see from (1) that $\lambda_{1}>0$ because the assumption $u(c_{i})>0$. Now, here comes the interesting part if $\frac{w^{'}(h^{*})}{1+r}-1>0$ implies that $\lambda_{4}=0$ by (3). Not always this would be the case, for example suppose that $w(h)=h(1+v)$ where $v$ is the return of investment in $h$. $\frac{w^{'}(h^{*})}{1+r}-1$ would be $ \frac{v-r}{1+r}$. If $v>r$ then $\frac{w^{'}(h^{*})}{1+r}-1>0$ and $\lambda_{4}=0$. But if $v<r$ then $\lambda_{4}>0$ by (3) and $h=0$ by (7).

This means that the optimal choice of h depends on this condition. If the return of h is bigger that his cost of oportunity (including r), then $h>0$ and would be a constant.

Now let's rule out the posibility that $c_{2}>0$. If this is true, $\lambda_{3}=0$, which by (2) implies that $\lambda_{1}=0$, which implies by (1) that $u^{'}(c_{1})=0$ that generally it's not true. So our assumption that $c_{2}^{*}=0$ it's in general correct.

So all this observations lead us to the following equations:

\begin{align}

u^{ ' }(c_{1}) = \lambda_{1} \ (8)\\

\lambda_{1}=(1+r)\lambda_{3} \ (9)\\

\frac{ w^{ ' }(h)}{1+r} = 1 \ (10)\\

c_{1}^{*} = y-h + \frac{ w(h)}{1+r} - \frac{1}{1+r} (11)

\end{align}

(8) comes from (1), (9) from (2), (10) from (3), and (11) from (4). From this system of equations the solutions to all the endogenous variables are obtained for $c_{1}^{*}$ is (11) and for $h$ is (10). So $\beta=0 \ \Rightarrow \ c_{2}=0$. Why $h_{*}>0$? This happens because investing in $h$ increases the NPV, so increases the consumption today, so invest in h increases utility in period 1.This does not depend on $\beta$, because it's a monetary relationship. But note that if the return of $r$ is greater thatn $h$, then it could happen that $h^{*}=0$.