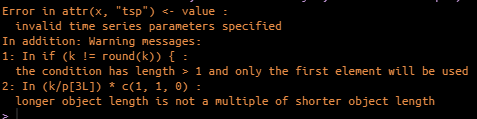

I have the following problem with the Arellano and Bond (1991) or Blundell and Bond (1998) estimators in R using the plm package. I receive the following problem when trying to run the needed regression:

The dataset could be found here: https://drive.google.com/file/d/1WUCrMCi7bJmhYbzZxNuXDpFIwXJTqdh3/view?usp=sharing

My code is the following, it seems that I do everything correctly, the formula I need to be estimated is the following:

remove(list=ls())

library(plm)

library(dplyr)

library(ggplot2)

library(prodest)

library(estprod)

library(broom)

library(pdynmc)

pckg<-c("plm","readxl","dplyr","ggplot2", "broom","prodest", "estprod")

#install.packages(c("plm","readxl","dplyr","ggplot2", "broom","prodest", "estprod"))

lapply(pckg, require, character.only = TRUE)

# Set the working directory

setwd("C:/Users/vadya/Desktop/baka")

# Downloading the survey data

Data <- read.csv("test.csv", header=TRUE, sep=",")

str(Data)

Data$ID<-as.numeric(as.factor(Data$ID))

summary(Data)

DataA11 <- Data %>%

filter(NACE == 'A' & Year < 2013) %>%

filter(VA > 0, L > 0, FA > 0, M > 0, Turn > 0, TA > 0) %>%

mutate(ID = ID,

Year = Year,

l = log(L),

va = log(VA),

fa = log(FA),

m = log(M),

turn = log(Turn),

ta = log(TA),

ff1 = (LTD + STD)/TA,

ff2 = lag(Cash),

ff4 = FA/Sales,

ff5 = TFA/TA)

####################################################################################

mod2LP <- prodest::prodestLP(DataA11$turn, fX = DataA11$l, sX = DataA11$fa, pX = DataA11$m, idvar = DataA11$ID, timevar = DataA11$Year,

R = 100, cX = NULL, opt = "optim", theta0 = NULL, cluster = NULL, tol = 1e-100, exit = FALSE)

mod2LP

omegaLP <- prodest::omega(mod2LP)

summary(mod2LP)

summary(omegaLP)

DataA11$omega <- prodest::omega(mod2LP)

######################################################################################

DataA11 <- DataA11 %>%

arrange(ID, Year) %>%

group_by(ID) %>%

mutate(domega = omega - dplyr::lag(omega),

debt = LTD + STD,

ddebt = debt - dplyr::lag(debt),

dsales = Sales - dplyr::lag(Sales)) %>%

ungroup

PDataA11 <- pdata.frame(DataA11, index = c("ID","Year"))

pdim(PData)

pvar(PData)

z1 <- pgmm(domega ~ lag(domega, 1:2) + ddebt + ff1 + ff1:ddebt + Age + ta + dsales | lag(domega, 2:99),

data = PDataA11, effect = "twoways", model = "twosteps")

summary(z1, robust = TRUE)

ALSO! It would be perfect if you provide any information on that package and also what I do incorrectly + would be great if you said how to add fixed effects to this pgmm function.

Thanks a lot to each of you in advance!!!:)

UPDATE:

data("EmplUK", package = "plm")

## Arellano and Bond (1991), table 4 col. b

emp.gmm <- pgmm(log(emp)~lag(log(emp), 1:2)+lag(log(wage), 0:1)+log(capital)+

lag(log(output), 0:1)|lag(log(emp), 2:99),

data = EmplUK, effect = "twoways", model = "twosteps")

summary(emp.gmm)

I run this code, that is provided here: https://rdrr.io/cran/plm/man/pgmm.html

and I get the following message:

nmust be a nonnegative integer scalar, not an integer vector of length 2. Then I filtered to get only the positive numbers (which is not logical) and got the next issue: Error in Formula(formula) : inherits(object, "formula") is not TRUE. So, I do not really know how to solve it, despite the fact I have read the documentation of the package. $\endgroup$