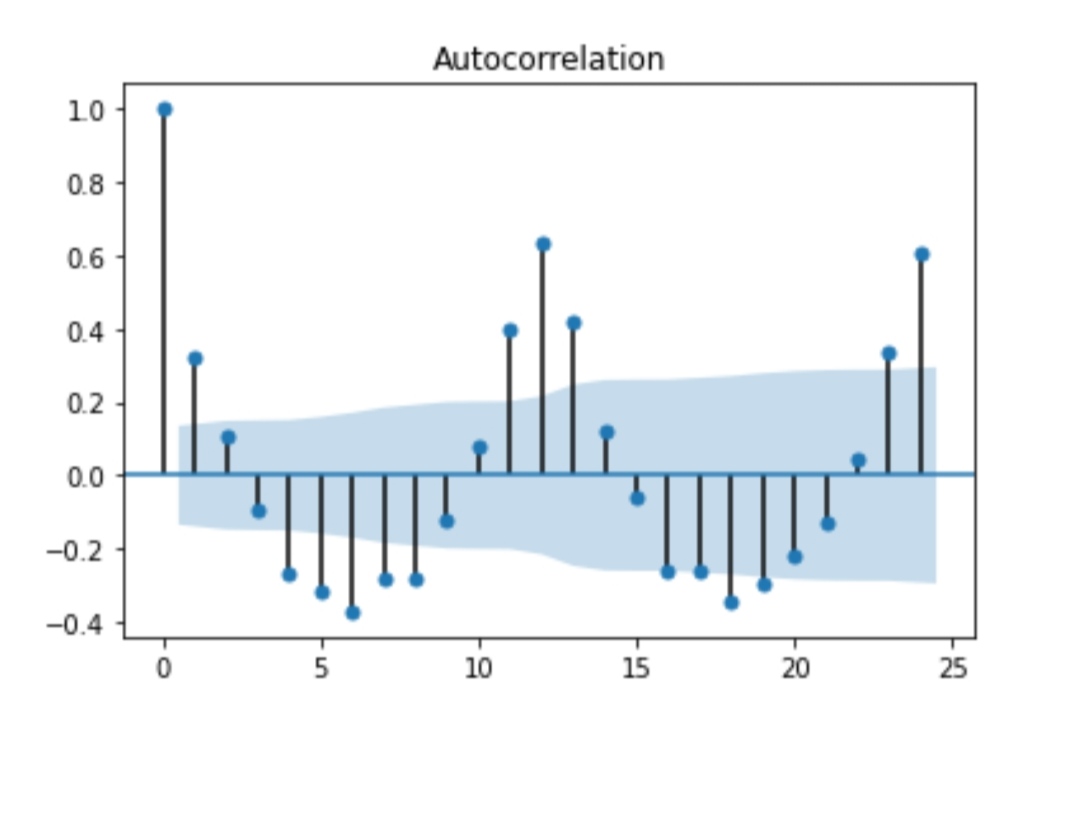

I have plotted an ACF plot and found all its lagged variables exceed the confidence interval range. I have tested again with Ljung box test on its residuals and most of the lagged variables have a significant test statistics to reject null hypothesis (i.e. p k = 0). In the end result, I get an AR(1) model given that the PACF test statistic is significant at lag 1.

What I confused is that why we don't include MA terms here although ACF test statistics are mostly significant. It contradict with what I thought ONLY DON'T include MA terms if the ACF test statistics of the lagged variables are NOT significant (or does not exceed confidence interval).