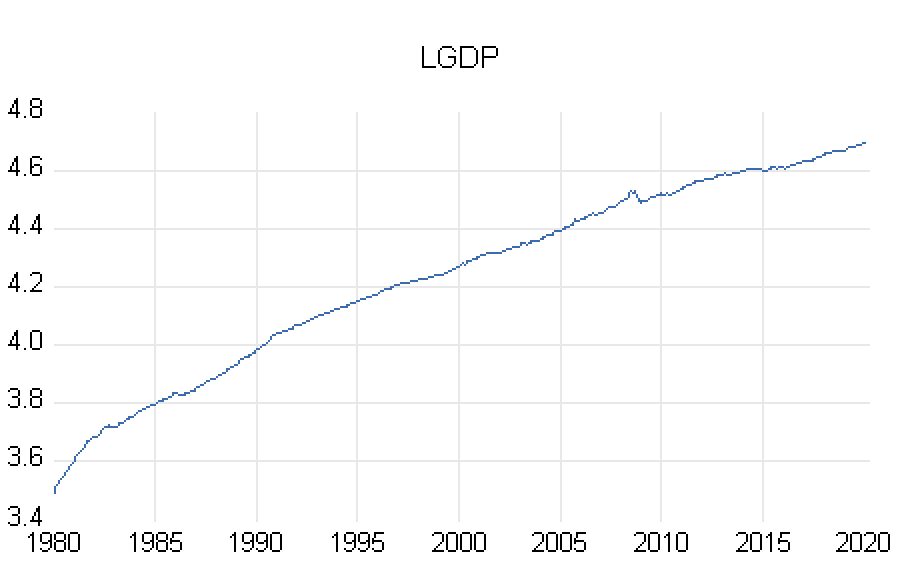

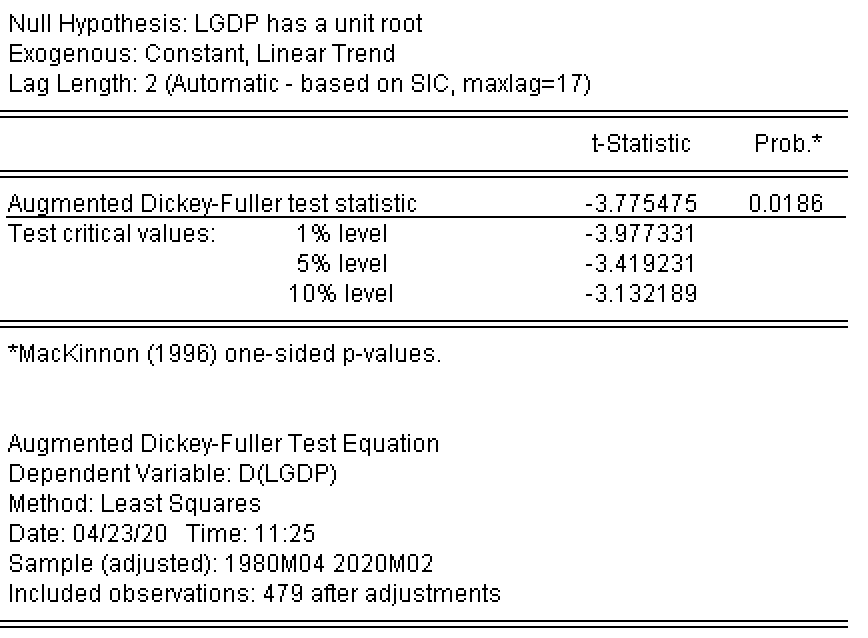

I think the source of your confusion may be due to the inclusion of the linear trend term in your test. If you exclude the linear trend from the test then you will almost certainly find evidence of a unit root. There is actually an open debate as to whether GDP is trend stationary (i.e. stationary once you remove the linear trend) or difference stationary (i.e. stationary once you take a difference of the series). For example, see: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=866624

To help you better understand it is possible to illustrate this with a simple model with a lag and a trend (this also generalizes for two lags but it is good to keep things simple). Consider the following model of GDP:

$y_{t}=\alpha+\beta y_{t-1}+\gamma t+e_{t}$

If we subtract $y_{t-1}$ from both sides we get that

$\Delta y_{t}=\alpha+(\beta-1) y_{t-1}+\gamma t+e_{t}$

where the null hypothesis of our unit root test is that $(1-\beta)=0$. The test depends on whether we account for the constant ($\alpha$) and the linear trend ($\gamma$) or not. If the true process has a linear trend but $\beta<1$ then you will not detect a unit root when including a linear trend in the test. On the other hand if you estimate the model without a linear trend and conduct the unit root test without an exogenous linear trend then the unit root test should not reject the null since the estimate for $\beta$ will move towards 1 to try and capture the linear trend. For this same reason if you have large structural breaks in the data the estimate of $\beta$ will move towards 1 and suggest evidence of a unit root (regardless of an inclusion or a linear trend or not).

Long story short if you include the linear trend in the test even if you exclude it from the estimated regression model then you are unlikely to find evidence of a unit root in an empirical process where a linear trend dominates unless the data were even more non-stationary than it appears.