I like @Steven Landsburg's point about inflation as another form of taxation, and thinking through how the government responds to having this new revenue source.

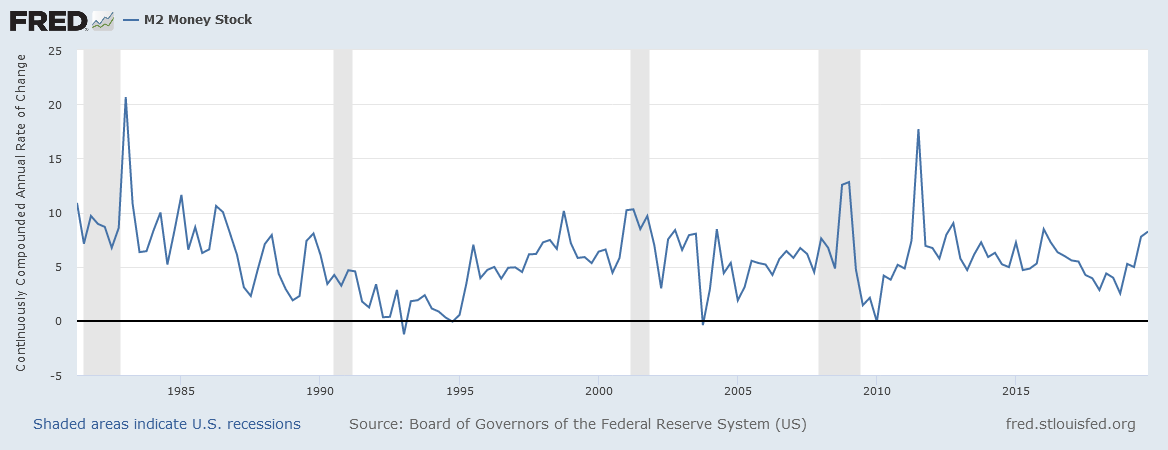

I'd like to make narrower monetary point. I'm not sure there is anything special about the trillion dollar coin that wouldn't be true for the federal government minting or printing an extra trillion in other coins and paper bills. FRED reports that there is about \$1.8 trillion worth of currency in circulation, so in some sense we would go from having an M0 of \$1.8 trillion to one of \$2.8 trillion. Which sounds like a pretty big change, but when you consider that most money is not in the form of currency but rather in bank deposits (almost \$16 trillion), perhaps the effects would be better measured by assuming a change in the broader money stock of \$1 trillion / \$M2, or about 6-7%. Yes, that's large for a given year, but not actually a huge rate of change relative to historical experience:

The general monetary rule of thumb is that prices are roughly proportional to the money supply (the neutrality of money). This means we would expect an additional and unexpected 6% increase in the money supply to increase prices by 6%. There may be important distributional consequences that depend on what the government spends the money on.

Does the coin money have to be spent to trigger this inflation effect? I'm not sure. From Wikipedia:

The concept of striking a trillion-dollar coin that would generate one

trillion dollars in seigniorage, which would be off-budget, or

numismatic profit, which would be on-budget, and be transferred to the

Treasury, is based on the authority granted by Section 31 U.S.C. §

5112 of the United States Code for the Treasury Department to "mint

and issue platinum bullion coins" in any denominations the Secretary

of the Treasury may choose. Thus, if the Treasury were to mint

one-trillion dollar coins, it could deposit such coins at the Federal

Reserve's Treasury account instead of issuing new debt.

I believe the way the Treasury's bond issuance works is that when the account is in deficit (subject to statutory limitations) the Treasury issues bonds to keep the government spending in line with congressional appropriations. What follows is a discussion from the NY Times when the it looked like the government might run an extended budget surplus (U.S. Treasury: No Lending; With Big Budget Surpluses, Some See The End of New Bonds and Notes By Jonathan Fuerbringer)

Yet pressing relentlessly against the Treasury market's viability is

the expected size of budget surpluses compared with the amount of debt

maturing each year. When the surplus exceeds the amount of old

Treasury notes and bonds maturing, the government has no need to raise

more cash to operate. So it will have a hard time arguing that it

needs to keep selling new securities, including the 10-year note,

which has already replaced the 30-year Treasury bond as the benchmark.

I therefore suspect that there are standard processes that would translate the resulting surplus into reduced debt issuance (potentially including not rolling over some existing debt).

However, I suspect the more important change from a huge influx of cash would be a concern that the US government would repeatedly do this. This would change expectations about inflation, which could create a large shock to current prices. The rough idea is that if people expect there to be a lot more money printed in the future, then prices will be higher in the future (and rise faster than they would have), so buying things now, before prices rise, especially long lived assets and durable consumption goods becomes a good idea. The resulting shifting of demand through time and the big inflation shock can be particularly harmful and wasteful.

Historically, countries that have tried to use printing money to solve serious budget issues have experienced very high inflation and a massive decline in the external value of their currencies. For example, my understanding is that every historical episode of hyperinflation has debt monetization as the most important cause behind the episode.