I am doing an essay on how a sovereign debt rating downgrade to junk status affects the economy. I wanted to use a theoretical framework to think about it, and seeing as an increase in the interest rate is involved, I decided to use the IS-LM model. Please tell me if the following is correct or not. I think it's a bit unconventional to shift the LM curve when money demands shifts, but the reason why I do that is because output was not the driving force of the shift in money demand. As I understand it, if output increases, that increases money demand, which is a movement along the LM curve. However, in this case, investor confidence affects the interest rate directly, without an initial effect on output. That is why I have shifted the LM curve upwards.

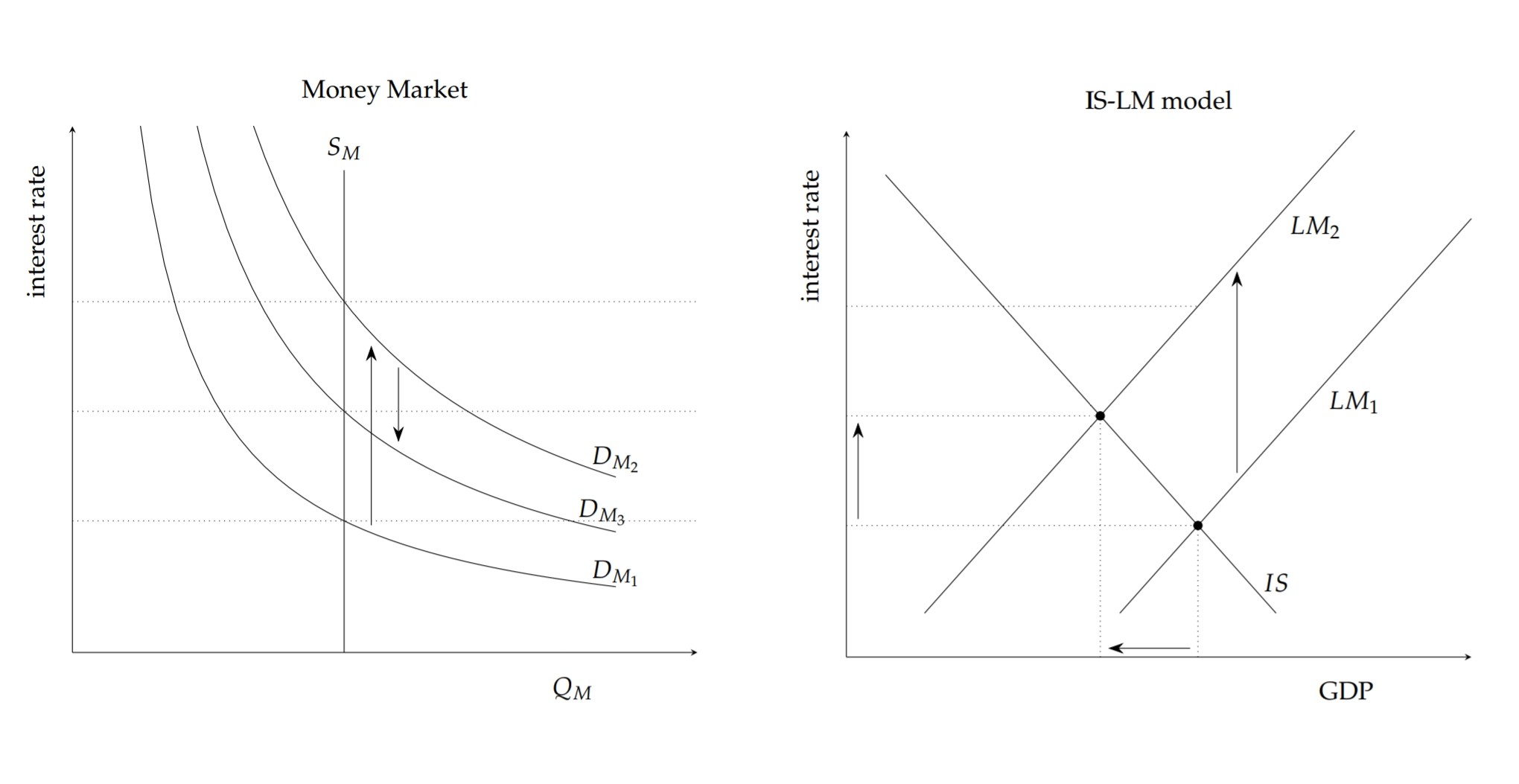

I presented the model as follows. Investor confidence drops with the news of a rating downgrade, so financial investors sell their bonds, which increases the demand for money, and decreases the prices of bonds. Because the prices of bonds decrease, interest rates on those bonds increase. Also, new bonds will have higher interest rates because they are seen as more risky. This is shown graphically in the money market model below as the first increase in money demand from $D_{M_1}$ to $D_{M_2}$. (I find it a bit confusing to think about foreign investors demanding more money (like M1), because I think they would want to sell the rand in exchange for their own currency, but I think this is true for the domestic economy.)

Because the money market is the basis of the LM relation, this shifts the LM curve upwards as the interest rate increases (shown as the increase from $LM_1$ to $LM_2$). Higher interest rates lead to lower real investment (i.e. investment in capital, land, labour and enterprise), government spending and consumption. This is equivalent to a movement upwards along the IS curve. The IS relation shows equilibrium in the goods market, which is given by $Y=C+I+G$. $I(i)$ is a (decreasing) function of the interest rate, and the interest rate increasing is what causes real investment to drop. It is a negative relationship because higher interest rates make it harder to borrow money to finance investments. In our situation, government spending decreases because the cost of credit for them increases, but rising Treasury bond interest rates also raises other interest rates throughout the economy due to competition, which then reduces private investment. The result is a decrease in the growth rate of output. The drop in output actually dampens the increase in the demand for money, because income decreases. So, the hike in interest rates is attenuated as output growth slows down. This can be reflected in the money market as a downwards shift in the demand for money curve from $D_{M_2}$ to $D_{M_3}$.

Another thing I want to check is if it is fine to think of there being only one interest rate in the graph on the left, due to the way central bank interest rate and other financial instrument interest rates rise due to arbitrage. The interest rate on Treasury bills is obviously what is affected, so is it fine to think of the demand for 'money' (is that demand for all the money in the entire economy?) as interacting with that interest rate?

I presume that reduced investor confidence is a fairly standard problem to model, yet I'm not so sure about how I've done it.