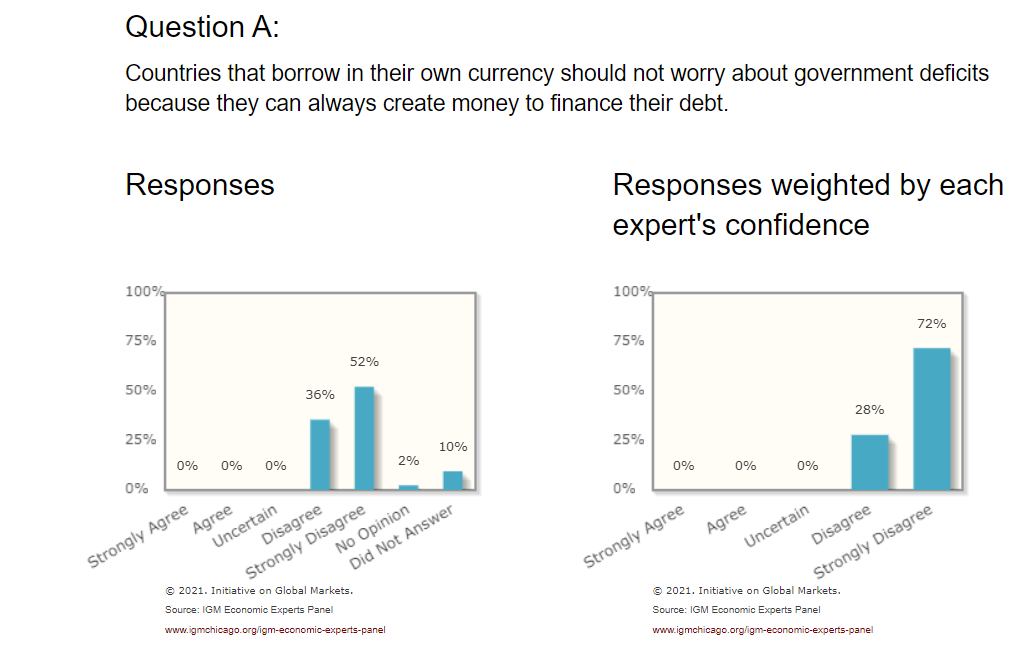

According to advocates of MMT, the primary risk once the economy reaches full employment is inflation, which can be addressed by gathering taxes to reduce the spending capacity of the private sector.

This statement is in accord with MMT, and it can be traced back to the concept of Functional Finance. One could do a search for Abba Lerner’s articles on Functional Finance to see the roots of the idea. There are theoretical differences between Functional Finance. L. Randall Wray’s working paper #900 at the Levy Institute discusses this.

Deflation is not seen as a risk because the Government of any country with sovereign control of its own internationally accepted currency can print money to create as much inflation as it wants at will (depending on who receives that money).

MMT rejects the concept of “printing money” as is understood by mainstream economics, and certainly rejects Monetarist notions about a linkage between money supply and the price level. Instead, deflation is not a worry as fiscal policy can be loosened.

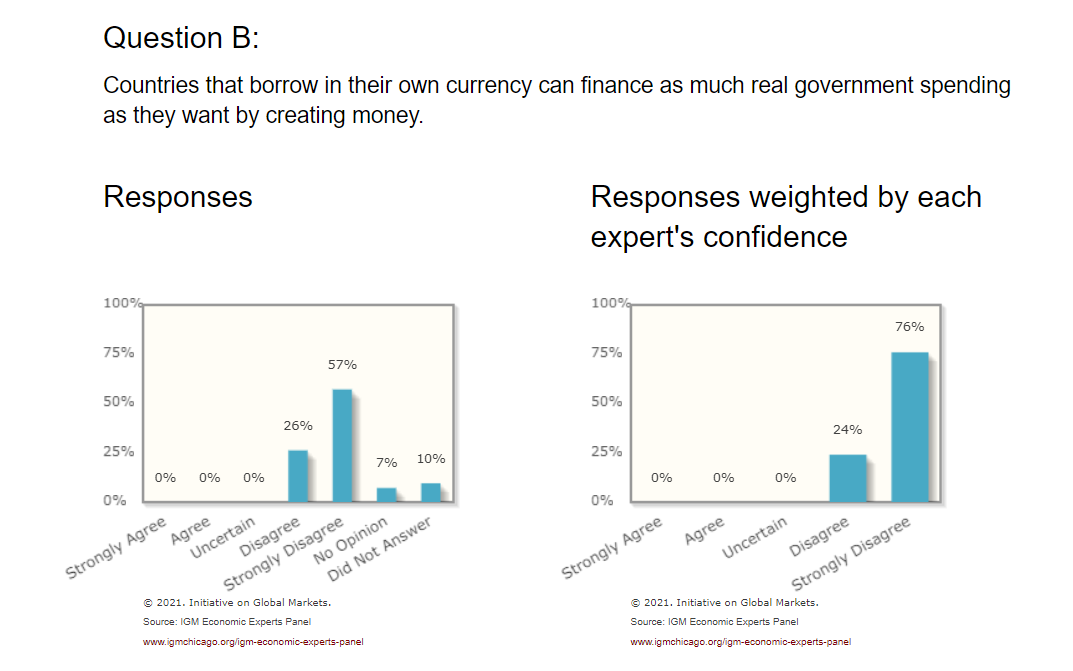

To add to the previous point: there is a difference between fiscal spending (e.g., handing households \$1 trillion) versus “quantitative easing” (the central bank buying \$1 trillion in existing bonds, which increases the money supply and reduces bonds held by the public). The difference should be obvious: handouts create an income flow, the second is just a secondary market financial transaction. MMT proponents argued that QE accomplishes almost nothing, saying that it is just a swap between two types of government liabilities. It should be noted that some neoclassical economists have made the same observation.

Since MMT proponents argue that QE accomplishes nothing, it is very hard to understand why some critics argue that MMT is just advocacy of “monetary financing.”

If we turn to page 343 of “Macroeconomics” by William Mitchell, L. Randall Wray, and Martin Watts (Wray & Mitchell are leading authorities on MMT, considered co-founders along with Warren Mosler) the authors state: “...when MMT says that government spends by keystrokes, this is a description, not a prescription. If critics were correct that government spending by printing money necessarily leads to high inflation or hyperinflation, then most developed nations would have at least high inflation, if not hyperinflation all the time because they all spend by keystrokes.”

It appears to me that this must be true to some extent, but my concern is that the feedback mechanism where the extra money generates inflation might not be smooth and free flowing for various reasons and a vast excess of money might accumulate in an unstable way in certain areas of the economy. After a period of time some trigger event might cause a sudden uncontrollable cascade flood of that money that could destroy public confidence and the currency itself. Is this an unfounded fear?

The issue is not money printing, rather too loose fiscal policy. The MMT argument is that you avoid this by structuring fiscal policy properly. For example, the key counter-cyclical policy proposed is a Job Guarantee. The Job Guarantee (JG) offers a job at a fixed wage. The JG wage acts as a de facto minimum wage, and so long as it is not increased, should not create upward pressure on wages. If the economy is seen to be overheating, workers will be bid away from the programme. This reduces the wages paid and increases income taxes - i.e., tightening fiscal policy automatically.

Arguably, bad policies - such as was pursued by mainstream Keynesian economists in the 1960-70s can create inflationary pressure. Fiscal policy needs to be tightened to avoid inflationary pressures if regulatory measures are not enough.

The fear of a “cascade” probably refers to fear of hyperinflation. The textbook “Macroeconomics” explains in Chapter 21 how mainstream theories about hyperinflation are incorrect in that they blame monetary financing. Instead, if we look at real world cases, hyperinflation is typically the result of the impairment of real productive resources. In the case of Weimar, there were gold reparations as well the occupation of the Ruhr.

However, these questions are really about a couple of topics that are misunderstood or misrepresented by other economists. The question title asks whether MMT offers insights into managing the economy. To answer that requires switching to topics not discussed within the question. For example, the Job Guarantee has nothing to do with “monetary financing.”

The previously mentioned textbook would be a good starting point to learn about MMT, or there are many resources online.